The waiting room of Denver’s Social Security Administration field office on Stout Street doesn’t invite conversation. Plastic chairs. A number-ticket dispenser. A flat screen cycling through benefit reminders nobody reads. It was a Tuesday in late February 2026 when I arrived to follow up on a separate story about SSA processing delays, and that’s where I first noticed Brittany Quintero — sitting two seats down from me, holding a manila folder on her lap and staring at the floor with the particular stillness of someone rehearsing a hard conversation in their head.

We started talking when her number didn’t get called for over an hour. By the time it finally did, she had told me enough that I asked if I could follow up properly. She said yes, though not without hesitation. “I don’t usually talk about money,” she told me later by phone. “People either judge you or try to sell you something.”

A Life Built on Steady Work — and a Marriage That Left Landmines

Brittany Quintero is 62 years old and has spent the better part of two decades as a union electrician in the Denver metro area, pulling consistent wages through Local 68 of the International Brotherhood of Electrical Workers. She’s not someone who stumbled into financial trouble through recklessness. Her problems arrived through the kind of slow, hidden accumulation that only surfaces when a marriage ends badly.

When Brittany and her then-husband divorced in late 2023, she believed the financial split was clean. She had her union pension contributions, a modest savings account, and about $47,000 in federal student loan debt from a graduate program in construction management she completed in 2019 — a degree she pursued hoping to move into project supervision. What she didn’t know was that her ex-husband had opened three credit accounts in both their names without her knowledge, running up roughly $23,400 in debt across two years.

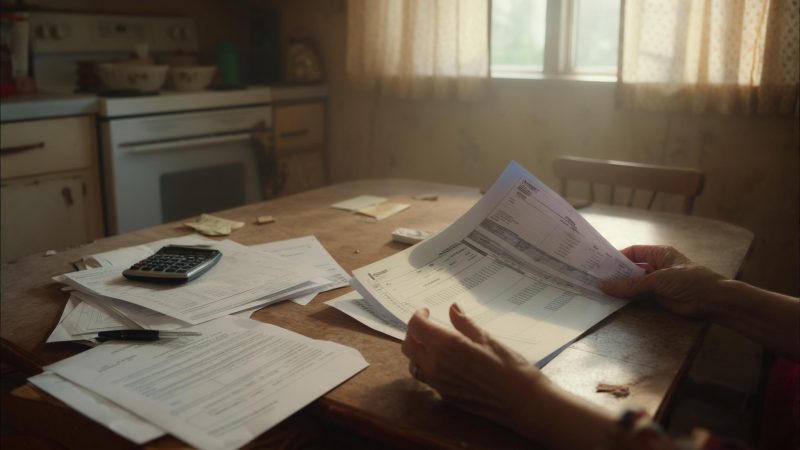

The collections notice arrived in January 2026, three months after her car — a 2014 Ford F-150 she relies on to reach job sites — broke down with a transmission failure estimated at $3,200 to repair. Without the truck, she had been cobbling together rideshares and borrowing a coworker’s vehicle when possible. She was, as she put it, “bleeding from three places at once.”

The Early Social Security Question — and Why It’s More Complicated Than It Sounds

The reason Brittany was in that SSA office comes down to one number: 62. Under current Social Security rules, 62 is the earliest age at which most workers can begin claiming retirement benefits. For someone in Brittany’s position — cash-strapped, with mounting debt and an unreliable work situation — the appeal of an immediate monthly check is obvious.

But early claiming carries a permanent cost. Because Brittany was born in 1964, her full retirement age is 67, according to the Social Security Administration’s retirement age chart. Claiming at 62 means her benefit would be reduced by approximately 30 percent — for the rest of her life.

The difference — roughly $575 per month — compounds dramatically over a long retirement. But Brittany wasn’t thinking in decades. She was thinking about whether she could make rent in March while waiting for her union hall to place her on the next available job.

As she explained it to me: “I know waiting is smarter on paper. But paper doesn’t pay my phone bill.”

The Student Loan Problem Nobody Warned Her About

There’s a wrinkle in Brittany’s Social Security calculation that she hadn’t fully understood before walking into that SSA office, and it’s one that surprises many people her age.

Under the Treasury Offset Program, the federal government can withhold up to 15 percent of Social Security benefits to recover defaulted federal student loans, according to the U.S. Department of the Treasury. Brittany’s $47,000 in graduate school debt is federal, and while her loans were technically still in repayment, she had missed four consecutive monthly payments by the time we spoke — a direct result of the financial cascade triggered by her car breakdown and the surprise collections debt.

The SSA representative she finally met with didn’t give her specific guidance on what to do, but did confirm that if her loans reached default status, her benefit payments could be reduced at the source. That detail landed hard. “I thought Social Security was mine,” she told me. “I paid into it for 20 years. I didn’t think someone could just take a piece of it.”

She left the office with more questions than she came in with — which is, honestly, the experience of a large share of the people I’ve spoken with in SSA waiting rooms over the years. The information is technically available through SSA’s online portal, but navigating it alone while managing a financial emergency is a different matter entirely.

What Brittany Decided — and What She’s Still Figuring Out

When I followed up with Brittany by phone in mid-March 2026, she had made one firm decision and was still wrestling with the rest. She had not filed for Social Security. A coworker’s referral had connected her with a HUD-approved nonprofit credit counselor in Denver who was helping her assess whether loan rehabilitation — a nine-month process — made sense before she made any moves on benefits.

The car situation had found a temporary patch — her union local had an informal ride-share arrangement she hadn’t known about, and a fellow electrician was picking her up four days a week in exchange for Brittany covering his lunch on job sites. It was an unglamorous solution, but it was keeping her employed.

The hidden debt dispute was murkier. A consumer protection attorney she consulted on a free initial call told her that if accounts were opened without her knowledge or consent, she might have grounds to dispute liability — but it would require documentation, time, and possibly litigation. “I’ve been burned by trusting the wrong person already,” she told me. “Now I’m supposed to trust a whole legal system to sort it out.”

The Bigger Picture Behind One Woman’s Waiting Room Visit

Brittany’s situation isn’t unusual in its basic shape. According to the SSA’s Annual Statistical Supplement, a significant share of workers claim Social Security benefits at 62 — the earliest possible age — often because financial pressure leaves them few alternatives. The permanent reduction in benefits that results is one of the more consequential and least-discussed features of the U.S. retirement system.

What made Brittany’s case distinct was the layered nature of her crisis. The student debt, the hidden marital debt, and the vehicle breakdown weren’t independent problems — each one was making the others harder to manage. Missing loan payments because of the car repair cost put her closer to default. Default threatened her Social Security income. And not being able to claim Social Security yet kept her in a cash deficit that left everything else fragile.

When I asked Brittany what she wished she’d known earlier, she didn’t hesitate. “That the system doesn’t talk to itself. The SSA doesn’t tell you about the Treasury offset thing. Your loan servicer doesn’t warn you it could hit your retirement check. You find all of this out when it’s almost too late.”

She wasn’t bitter about it in the way you might expect. There was more resignation than anger — the particular exhaustion of someone who has learned that navigating government programs requires a kind of vigilance that nobody formally teaches you. Brittany is still working, still showing up, still rebuilding. Whether the decisions she’s making now will look wise or costly in five years, she honestly can’t know yet. Neither can I.

What I can say is this: when I left that SSA waiting room in February, Brittany was still sitting in her plastic chair, folder in hand, waiting for her number. And she was still there an hour later when I walked back through to leave. She waved. I waved back. Some waits, it turns out, are about a lot more than paperwork.

Leave a Reply