The first thing Deshawn Parker showed me when I sat down with him at a coffee shop near Detroit’s Midtown district was his phone — open to a credit monitoring app, a number in the low 500s glowing on the screen like an accusation. He set it face-down on the table almost immediately, as if closing the app could make the number go away. “I built something real,” he said. “And then one night in an ER undid a lot of it.”

Parker is 27 years old, a self-taught graphic designer whose client work spans brand identities, album artwork, and digital campaigns for small businesses across Michigan. He’s genuinely talented — his portfolio reads like someone who’s been doing this for fifteen years, not five. But talent doesn’t make quarterly estimated taxes easier to calculate, and it doesn’t provide a health insurance card when your appendix decides to rupture on a Tuesday night in October 2024.

Leaving the Warehouse — And the Safety Net That Came With It

Parker spent three years working a logistics warehouse job that paid roughly $38,000 annually. It came with employer-sponsored health insurance, a predictable schedule, and zero creative satisfaction. By early 2023, he’d built a freelance client base substantial enough — he thought — to make the leap. His first full year freelancing, 2023, netted him approximately $41,000 in gross income. Not a dramatic upgrade, but it was his.

What he didn’t fully account for was the volatility. When I asked him to describe what income variability looks like month to month, he didn’t hesitate. “January this year I made $4,200. February I made $810. Like, those are real numbers. That’s not me exaggerating.” The swing between feast and famine is a structural feature of freelance design work, not a bug — large project payments arrive irregularly, retainer clients churn, and slow seasons can compress three months into a single painful stretch.

He also didn’t immediately enroll in a health plan through the ACA Marketplace after leaving his warehouse job. He looked at the premiums, felt confident he was young and healthy, and decided to go uninsured for what he described as “just a few months until I stabilized.” Those few months stretched to over a year.

The Night Everything Shifted

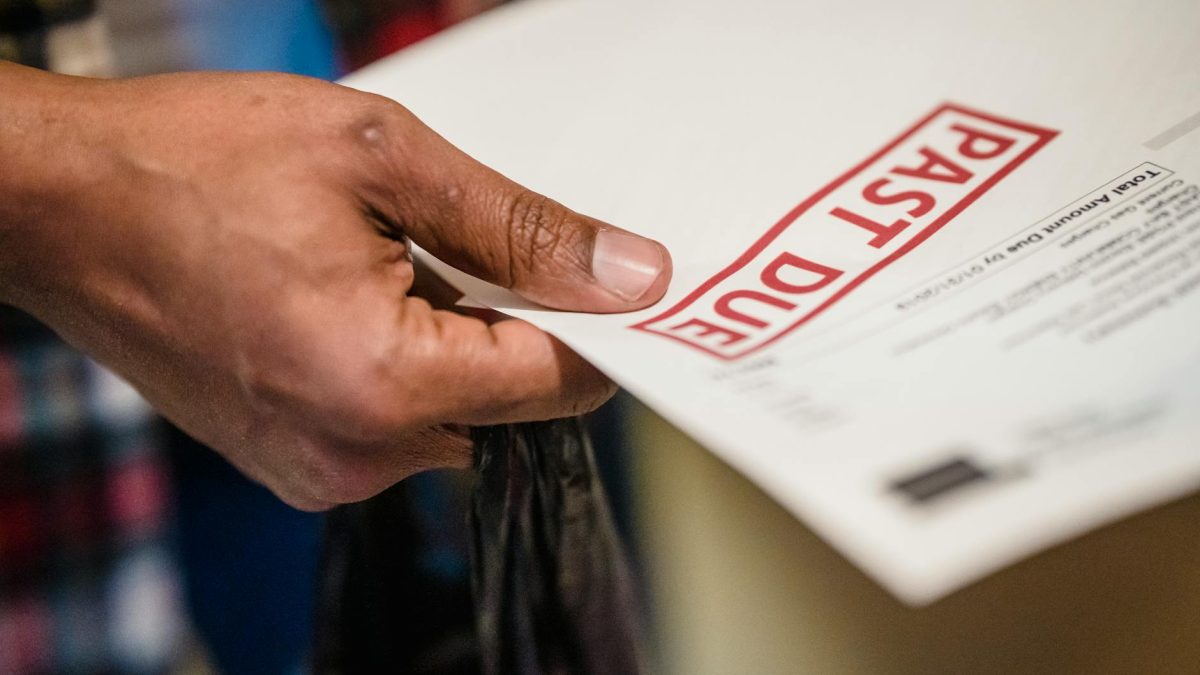

On October 14, 2024, Parker woke up at 2 a.m. with what he initially assumed was food poisoning. By 4 a.m., the pain had localized sharply enough that he had a neighbor drive him to the Henry Ford Hospital emergency room in Detroit. Surgeons removed his appendix that morning. The procedure was textbook — he was discharged the following afternoon. The bill was not textbook.

The hospital’s itemized statement arrived in late November: $14,230. Because Parker had no insurance, he was billed at the uninsured rate — a figure hospitals are not legally required to reduce, though many have charity care programs that can dramatically lower what an uninsured patient owes. Parker told me he didn’t know that. “Nobody at the hospital told me to ask about financial assistance,” he said. “I got a bill, I panicked, I ignored it, and then it was gone to collections before I even understood I had options.”

The account was sold to a third-party collections agency by January 2025 — roughly 75 days after the bill was issued. That collections entry hit his credit report in February 2025 and dropped his score by an estimated 80 to 100 points. He’d had a 610 before; he woke up to a 519.

What Relief Actually Existed — And What He Missed

When I started walking through the economic relief landscape with Parker, the picture that emerged was genuinely complicated. Several programs could have meaningfully helped him — some before the ER visit, some after — but each had its own eligibility windows, application timelines, and bureaucratic friction that made them easy to miss for someone without a dedicated benefits counselor.

The most significant missed opportunity was the ACA Premium Tax Credit. Based on Parker’s 2023 income of approximately $41,000 — roughly 280% of the federal poverty level for a single adult — he would have qualified for a substantial subsidy on Marketplace health coverage. According to the Kaiser Family Foundation, a 27-year-old at that income level in Michigan could have accessed a benchmark silver plan for as little as $150 to $200 per month after the tax credit. He was paying nothing — because he had no coverage at all.

There was also the matter of Michigan’s Medicaid expansion. Parker’s income in the months before his surgery had dipped significantly — he told me that September and early October 2024 were particularly slow, with only about $1,400 in documented income across both months. At that annualized rate, he may have qualified for Michigan’s Healthy Michigan Plan, which covers adults up to 138% of the federal poverty level. He never checked.

The Ongoing Reckoning With Irregular Income

Beyond the medical debt, I wanted to understand how Parker manages the fundamental instability of freelance income — because the insurance gap didn’t happen in isolation. It happened because he was trying to conserve cash during a period of financial uncertainty, and a $150 monthly premium felt like a luxury he could defer.

“The problem is that when money is coming in, I spend like it’s going to keep coming in,” Parker told me, with the directness of someone who has spent a lot of time diagnosing his own patterns. “And when it stops, I’m already behind. There’s no buffer. There never has been.”

This volatility creates a specific kind of bureaucratic problem: income-based program eligibility is typically calculated on an annual basis, but a freelancer’s financial reality shifts month to month. Parker projected a $45,000 income year when he enrolled in Marketplace coverage in November 2024 — yes, he finally enrolled, after the surgery — but his actual income for the remainder of 2024 came in closer to $28,000 due to the medical disruption slowing his work. That discrepancy will affect how his Premium Tax Credit reconciles when he files his 2024 taxes.

Where Deshawn Parker Stands Now

When I spoke with Parker in late March 2026, he had been enrolled in an ACA Marketplace plan for sixteen months. His current premium, after the Premium Tax Credit based on a projected $36,000 annual income, runs $187 per month. He considers it the most important bill he pays. “I look at that charge come out every month and I’m not even mad about it anymore,” he said. “I’m relieved it’s there.”

The $14,000 collections account is more complicated. He negotiated a settlement with the collections agency in September 2025 for $6,800 — roughly 48 cents on the dollar — which he paid using a combination of savings and a payment from a large brand identity project. The collections entry will remain on his credit report until approximately 2031, seven years from the date it was first reported, under standard Fair Credit Reporting Act rules. His score, as of this month, has climbed back to approximately 562.

He is, in his own words, rebuilding. His gross income in 2025 came in at approximately $48,000 — his strongest year yet. He has a small emergency fund for the first time, around $2,100, which he describes with the kind of pride usually reserved for much larger accomplishments. He knows it wouldn’t cover another ER visit. He knows he still has a credit score that makes apartment applications difficult. He is not, by any reasonable measure, financially recovered.

But he is insured. And he is still designing.

What stays with me after my conversation with Deshawn Parker is not the dollar amounts — though the math is brutal enough on its own. It’s the architecture of how these gaps work. He was never reckless. He was self-employed, young, and navigating a system that offers meaningful relief to people who already know it exists. The programs were there. The subsidy was there. The hospital’s financial assistance policy was there. None of it reached him in time to matter.

“I wish someone had just handed me a list,” Parker told me as we wrapped up. “Not advice. Just — here are the things that exist. Here are the deadlines. That’s all I needed.”

Leave a Reply