Waiting for a government check that has not been authorized by Congress is not a financial strategy — it is a gamble, and the people with the least margin for error are the ones most likely to lose. That uncomfortable truth sits at the center of Garrett Jennings’s story, and it is something I keep thinking about weeks after sitting down with him at a Milwaukee diner on a gray Tuesday in late March 2026.

I first encountered Garrett at the East Branch of the Milwaukee Public Library, where a community nonprofit had organized a free Medicare enrollment information session. I was there to report on retirement anxiety among workers approaching 65. Garrett, a 63-year-old school bus driver for Milwaukee Public Schools, had come with a notepad full of Medicare questions. But within minutes of the session wrapping up, he caught my eye near the exit and asked something that had nothing to do with Part A or Part B.

“Is that $2,000 check actually happening?” he said quietly, half-statement, half-question. “Because I’ve been making decisions based on it.”

I asked if he had time to talk. He did.

A Careful Man in a Precarious Position

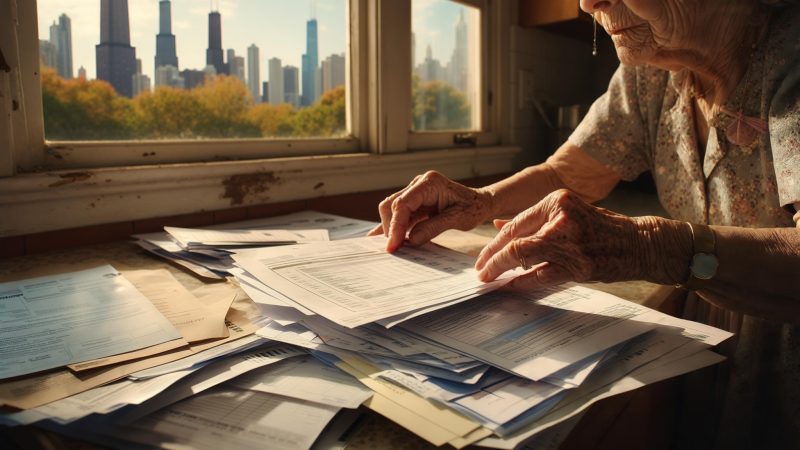

Over coffee two blocks from the library, Garrett walked me through his finances with the kind of methodical precision that comes from years of keeping close track of money that never quite stretches far enough. He has driven school buses for 17 years and earns approximately $52,000 annually. For the past eight years, he has also run a small weekend shuttle transport service — ferrying elderly clients to medical appointments and airport terminals — which once brought in an additional $900 to $1,100 per month.

Over the past year, that side income collapsed to roughly $350 a month, undercut by rideshare apps and rising fuel costs. One of his longest-standing clients, a 79-year-old woman he had driven to dialysis three times a week, had entered hospice care in February. That single loss had cut his March shuttle revenue to $210.

His mortgage on a three-bedroom home in Milwaukee’s Sherman Park neighborhood carries that $1,847 monthly payment. When he and his wife Denise bought the house in 2018, the math had worked. Denise, who retired in January 2026 after 31 years as a school librarian, had been earning a salary that helped absorb the shortfalls when the shuttle business slowed. Now on a fixed pension of approximately $1,640 per month, she is no longer a financial buffer.

“We’re not broke,” Garrett told me carefully, wrapping both hands around his coffee mug. “But we’re thin. Really thin. And Denise keeps saying we need to stop pretending we’re not.”

He had roughly $4,200 in savings — what he called his “break-glass fund.” He had not touched it. Yet.

Where the $2,000 Idea Came From

Garrett told me he first heard about the $2,000 stimulus check in February 2026 through a Facebook group for Milwaukee-area retirees and near-retirees. The posts cited a proposal from President Trump to distribute tariff revenue directly to American households — a concept being called a “tariff dividend.” By March, the idea had taken on a life of its own online, with some posts claiming checks would arrive in April 2026.

According to a Capitol Skyline fact-check on the April 2026 stimulus claim, no legislation authorizing a $2,000 payment has passed Congress, and no official distribution timeline has been established by any federal agency. The proposal exists — President Trump did float the concept of tariff-funded checks — but there is a significant gap between a presidential suggestion and a signed law with IRS disbursement instructions.

As Kiplinger reported in early 2026, the tariff dividend concept has drawn attention from economists and some lawmakers, but no bill has cleared both chambers of Congress. More than $166 billion in tariff revenue has been cited in discussions about funding such payments, but the mechanics of who would qualify, at what income threshold, and through which agency remain entirely unresolved.

Garrett had read the Facebook posts. He had not read the fact-checks. He had not looked up official IRS guidance or congressional records. He had, in his own words, “just assumed it was moving forward.”

“It seemed real,” he said. “The number was specific. People were talking about it like it was already done. I thought, okay, this is actually happening.”

The Decision That Kept Him Up at Night

In early March 2026, Garrett made a quiet calculation. His April mortgage payment would come due. His savings could cover it. But he told himself he would wait — hold the savings and see if the stimulus check arrived first. If it came, he would use it for the mortgage and keep his break-glass fund intact.

What he did not fully account for was the psychological weight of that waiting. He described the weeks between that decision and our conversation as grinding — checking his bank account each morning, refreshing news sites at lunch, feeling a low-grade shame he could not quite name. He is not a man prone to recklessness. He has driven the same route for 17 years. He shows up early. He knows every kid’s name on Bus 114.

Denise, he said, knew something was off but had not pressed him to name it. “She trusts me,” he said. “That makes it worse.”

What the 2026 Relief Landscape Actually Looks Like

Setting Garrett’s story aside for a moment, the broader landscape of 2026 economic relief is genuinely confusing — which is part of why people end up in his position. There are real payments happening in some places. There are real proposals circulating in Washington. The problem is that the two categories are getting blurred in social media discussions and viral posts.

A number of states have active rebate and relief programs in 2026. According to AOL’s 2026 state stimulus roundup, at least seven states are distributing rebate checks or direct relief payments this year, each with its own eligibility rules, income caps, and deadlines. Wisconsin, where Garrett lives, is not currently among them.

At the federal level, as CNBC reported in March 2026, a bill creating a tariff rebate program has drawn discussion but faces an uncertain path through Congress. The concept of tariff-funded household payments is real. The checks are not — not yet.

The confusion matters because Garrett is not an outlier. He is representative of a cohort of middle-income Americans in their early sixties — people who are not poor enough to qualify for most safety-net programs, not wealthy enough to absorb financial shocks easily, and increasingly susceptible to hopeful misinformation because the stakes feel so high.

Where Garrett Stands Now

When I spoke with Garrett again by phone in early April 2026, he had paid his mortgage — from savings. The check had not arrived, and he had accepted it was not coming in April, whatever might happen in Congress later in the year.

“I used $1,847 out of the break-glass fund,” he told me. “Which means I’ve got about $2,350 left. That’s the whole cushion now. For both of us.”

He was not angry. More resigned — the way someone sounds when they have made peace with a mistake without quite forgiving themselves for it. He said Denise had taken the news steadily. “She just said, ‘Okay, so what’s the plan?’” He paused on the phone. “That’s her. Thirty-nine years and she still gives me that.”

He is now exploring whether his shuttle service can be revived through direct outreach to assisted living facilities — a market segment he had never formally targeted. He expects to enroll in Medicare at 65 and is trying to make every financial decision based solely on money he can confirm is real.

What stayed with me after our conversations was not the dollar amount — $1,847 is serious, but survivable. It was the month of quiet erosion that preceded it. Garrett described low-grade financial anxiety that does not announce itself but chips away at your concentration, your sleep, your sense of stability. He drove 42 kids to school through every day of it, smiling at each stop.

The $2,000 tariff dividend may still become law. Proposals evolve, and the political appetite for direct payments has not disappeared. But as of today, Garrett’s experience is a sharp reminder that a widely circulated rumor — even a plausible one backed by real policy discussions — is not a deposit. And for people with $2,350 standing between them and financial freefall, the difference is everything.

Byline: Vivienne Marlowe Reyes, Senior Tax & Stimulus Writer, American Relief. This article is reported narrative journalism. Nothing in this story constitutes financial advice.

(function(){var w=document.getElementById(‘pvv-scenario-s17756569894744eqr’);if(!w)return;var btns=w.querySelectorAll(‘button[data-choice]’);btns.forEach(function(b){b.addEventListener(‘click’,function(){if(w.dataset.revealed)return;w.dataset.revealed=’1′;btns.forEach(function(x){x.style.opacity=x===b?’1′:’0.45′;x.style.cursor=’default’;x.style.transform=’none’});var o=document.getElementById(‘s17756569894744eqr-out-‘+b.dataset.choice);if(o){o.style.display=’block’}});b.addEventListener(‘mouseenter’,function(){if(!w.dataset.revealed){b.style.borderColor=’#38bdf8′;b.style.transform=’translateX(4px)’}});b.addEventListener(‘mouseleave’,function(){if(!w.dataset.revealed){b.style.borderColor=’#334155′;b.style.transform=’none’}})})})();

.pvv-faq-section details summary::-webkit-details-marker{display:none}.pvv-faq-section details summary::marker{display:none;content:””}.pvv-faq-section details[open] summary .pvv-faq-arrow{transform:rotate(90deg)}

Leave a Reply