The Detroit Public Library branch on Livernois Avenue was busier than I expected for a Tuesday afternoon in January 2026. Tables had been arranged near the reference section for a free Medicare enrollment assistance event, and a line of mostly older residents stretched past the periodicals shelf. I was there to report on how community health navigators were helping residents understand their coverage options — but the story I ended up writing wasn’t the one I had planned.

About forty minutes in, a woman in a burgundy fleece vest approached me with a spiral notebook and a look I recognized immediately: the particular exhaustion of someone who has been asking the right questions for a long time without getting useful answers. She had overheard me talking to one of the event coordinators and assumed, correctly, that I knew something about how these programs actually worked. “I just need to understand if I qualify for anything,” she said. “Because right now, everything I make goes right back out.”

That was my introduction to Glenda Parker.

A Home Health Aide Earning $54,000 — and Still Running Dry

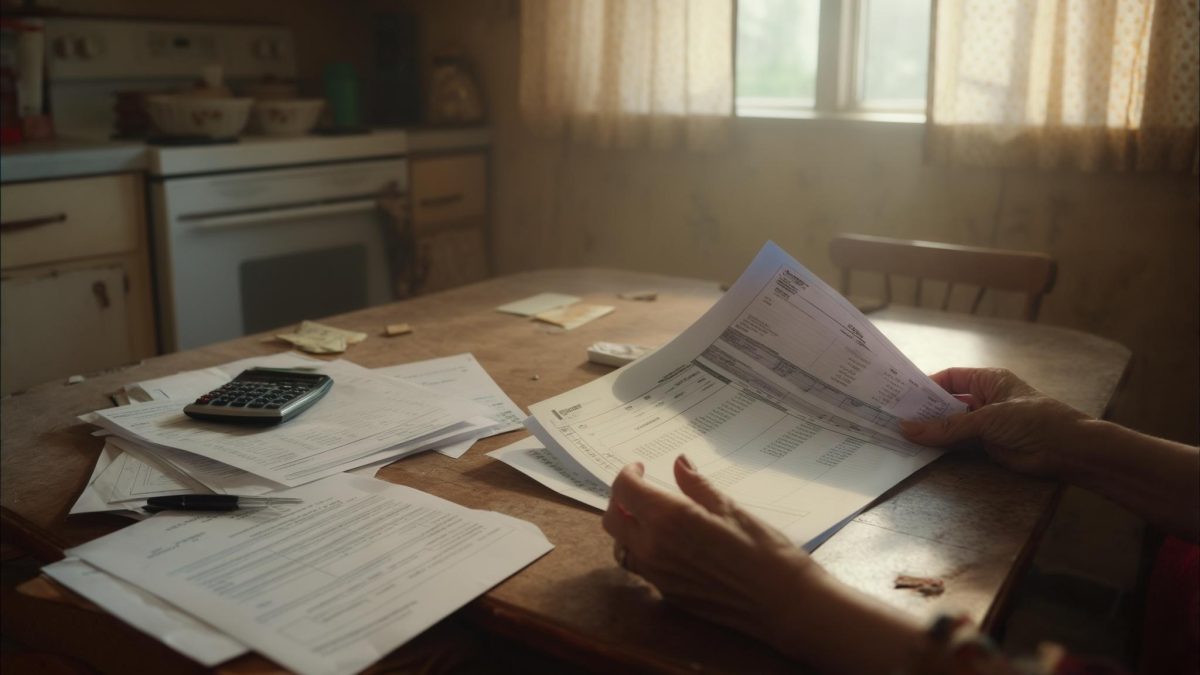

When I sat down with Glenda Parker at a corner table after the formal event ended, she spread her spiral notebook open to a page dense with handwritten figures. Glenda is 58 years old, divorced, and works as a home health aide through a Detroit-based placement agency that classifies its workers as independent contractors. She has been doing this work for eleven years. In 2025, she earned roughly $54,000 — a number that sounds stable until you trace where it actually goes.

Glenda pays $520 a month in child support for her 16-year-old daughter, who lives with her ex-husband in Southfield. She also contributes approximately $400 a month toward childcare costs for her 19-year-old son’s infant daughter — informally, without any legal arrangement, because her son works evening shifts and the cost of licensed daycare in Wayne County averages over $1,100 a month. “He can’t afford it and I can’t let the baby sit somewhere unsafe,” she told me. “So I fill the gap.”

Then there’s health insurance. Because her agency classifies her as a contractor, Glenda receives no employer-sponsored benefits. She has been purchasing coverage through the ACA marketplace for five years. In 2025, her monthly premium was $487 for a Silver plan with a $3,800 annual deductible. Add $1,200 in rent and utilities, transportation, and groceries, and Glenda’s fixed monthly outflow reaches roughly $2,850 — against take-home pay, after self-employment taxes, of approximately $3,700.

That leaves around $850 a month for everything else: car repairs, medical co-pays for her Type 2 diabetes and lumbar arthritis management, and whatever she contributes when her daughter calls with a need her father can’t cover. There is no emergency fund, no retirement account, and no buffer. “I make too much for Medicaid and too little for peace of mind,” Glenda said, and the numbers backed her up completely.

What Glenda Thought She Knew About Her Options

Glenda had come to the Medicare event with a specific question: could she qualify for Medicare before age 65 due to her disabilities? She has been managing Type 2 diabetes and chronic lumbar arthritis for several years — conditions that limit her ability to work long shifts and have required ongoing specialist visits costing her hundreds of dollars in out-of-pocket expenses annually. She had heard somewhere that Social Security disability recipients could access Medicare earlier than the standard eligibility age of 65.

She was partially right, but the path was longer than she knew. According to Medicare.gov, individuals under 65 can qualify for Medicare only if they have received Social Security Disability Insurance (SSDI) benefits for 24 consecutive months. Glenda had never applied for SSDI. She had been pushing through full shifts, reluctant to reduce her income or signal vulnerability to her placement agency.

The event coordinator — a licensed health navigator named Marcus Webb — walked Glenda through this clearly and without judgment. What emerged from that conversation, and what Glenda described to me in detail over the following hour, was a realization that she had been navigating the benefits system with incomplete information for years.

The Gap Between What She Paid and What She Could Have Paid

When Marcus pulled up the ACA premium tax credit estimator for Glenda’s income and household composition, both she and I leaned forward. At $54,000 a year, her income falls at approximately 230% of the Federal Poverty Level for a single-person household. At that ratio, her subsidy was modest. But Glenda has a 16-year-old dependent daughter — a fact that, if accurately reported, would shift her household to two people and push her FPL percentage meaningfully lower, increasing her available subsidy.

The problem was documentation. Glenda had been enrolling each year as a single individual without a dependent, because she is not the custodial parent. She assumed that since her daughter lives with her ex-husband, she couldn’t claim her. According to the IRS premium tax credit guidelines, a non-custodial parent can claim a child as a tax dependent if the custodial parent formally releases that exemption using IRS Form 8332. Glenda and her ex-husband had a verbal agreement that she would claim their daughter — but it had never been put in writing.

The Child Tax Credit alone — which the IRS caps at $2,000 per qualifying child under age 17 for tax year 2025 — could reduce Glenda’s annual tax liability significantly. She had never claimed it. “I didn’t think it applied to me because she doesn’t live with me,” Glenda told me. “I just assumed it was only for the parent she lives with.”

The Outcome — Partial, Complicated, and Honest

When I followed up with Glenda by phone six weeks after the library event, she had made two concrete moves. She had spoken with her ex-husband, who agreed to sign Form 8332, and she had scheduled an appointment with a Volunteer Income Tax Assistance (VITA) site in Detroit to amend her 2024 return and correct her 2025 marketplace enrollment status.

The revised ACA premium tax credit, once her household size is accurately reflected, is estimated to reduce her monthly premium from $487 to approximately $340 — savings of $147 a month, or roughly $1,764 annually. That is not a transformation. But for someone running $850 a month in discretionary room, $147 is the difference between handling a car repair and carrying it on a credit card.

The SSDI question remains unresolved. Glenda is not ready to file a claim. She worries, reasonably, that applying will signal unreliability to her placement agency — and she is protective of her income, even as that income strains her every month. “I know what I have,” she said quietly. “I don’t know what I’d have if I rocked the boat.”

The Child Tax Credit amendment is still pending as of this writing. If it clears for tax year 2024, Glenda may receive a refund of up to $2,000 — money she said she would put toward her daughter’s school expenses and a small emergency buffer she has never managed to build. She said this with the careful optimism of someone who has been disappointed by paperwork before.

What Glenda’s Story Reveals About a Larger Problem

Glenda Parker is not, by most definitions, a low-income American. She earns $54,000 a year, pays her taxes, and supports two generations of her family without complaint or public acknowledgment. But she has spent years in a coverage gap that doesn’t have a clean policy name — earning too much for expanded Medicaid, facing too much complexity to navigate the ACA correctly without professional help, and left with too little margin to absorb the errors that complexity produces.

She is not unique. Independent contractors, home health aides, and gig workers — a workforce that has expanded substantially over the past decade — frequently lack the HR departments, employer benefits, and professional tax support that help salaried employees optimize their relief eligibility automatically. The programs exist. The subsidies are real and available. Accessing them accurately, however, requires knowledge that is not evenly distributed.

- Approximately 16 million Americans work as independent contractors without access to employer-sponsored health benefits

- Home health aides represent one of the fastest-growing occupations in the country, with a median annual wage well below Glenda’s earnings

- VITA sites — free tax preparation services for qualifying individuals — operate in most major metro areas and can help correct prior-year filing errors

When I left Glenda at that library table in January, she was photographing Marcus Webb’s business card with her phone. She had three pages of notes and, for the first time in a while, the beginning of a plan. The money hadn’t changed yet. But the information had — and in her situation, that’s where it had to start.

Whether the plan holds — whether the paperwork clears, whether her ex-husband follows through with the form, whether the VITA appointment leads somewhere real — is something I will check back on. Glenda Parker has been filling gaps for other people for eleven years. She is practiced at it. The harder question is why she had to be.

Related: He Paid $374 a Month for Health Insurance on $34,000 a Year — Then One Phone Call Changed Everything

Related: Your IRS Refund Tracker Went Blank After Filing — Here’s What That Actually Means in 2026

Leave a Reply