The open enrollment deadline for ACA marketplace plans passed on January 15, 2026, but for many Americans, the real reckoning comes weeks later — when the first premium invoice of the new year arrives. That’s exactly when Tanya Dillard’s phone started buzzing with panic.

I first connected with Tanya in late January through a mutual friend, Marco, who mentioned her situation at a neighborhood barbecue in Tucson the week before. He described a woman who was organized, clear-eyed about money, and suddenly completely blindsided by a number on a piece of paper. I reached out, and she agreed to meet me at a coffee shop near her apartment on a Tuesday morning before she left for a three-day trip to Dallas.

A Number That Didn’t Make Sense

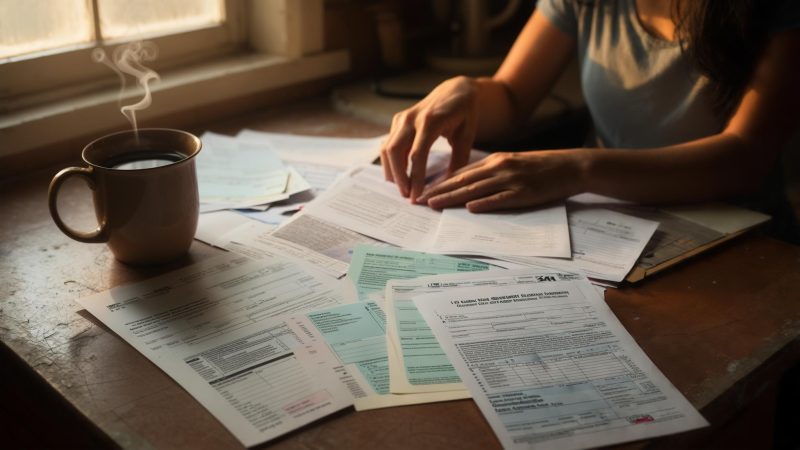

When I sat down with Tanya Dillard, the first thing she did was pull up a screenshot on her phone. It showed two figures side by side: her 2025 monthly health insurance premium of $487, and her 2026 renewal premium of $1,094. She had a 13-year-old daughter, no financial support from her ex-partner, and a student loan balance from a graduate degree that still sat at $64,500.

As a flight attendant earning roughly $81,000 a year, Tanya technically qualified as upper-middle income. But income on paper and income in practice are two different things when you’re the only adult in a household. After her mortgage, her daughter’s school costs, and her $718 monthly student loan payment, the math on a $1,094 insurance bill simply did not work.

“I actually sat on the floor of my kitchen for a minute,” Tanya told me. “I kept refreshing the page thinking it was a glitch. It wasn’t a glitch.”

The increase was real and, for many marketplace enrollees in Arizona, not unusual. Benchmark plan premiums in several Tucson-area markets rose sharply heading into 2026, partly due to insurer exits and partly due to shifts in the benchmark silver plan calculations that determine subsidy levels.

The Letter She Almost Recycled

In early December 2025, Tanya had received a letter from Healthcare.gov about her eligibility for an updated Advanced Premium Tax Credit for the coming plan year. She told me she put it on her kitchen counter next to the electric bill, then moved it to a drawer, then almost lost it entirely when she cleaned before the holidays.

The Premium Tax Credit, established under the Affordable Care Act and expanded through subsequent legislation, is designed to reduce monthly insurance costs for households whose income falls within a specific range relative to the federal poverty level. According to Healthcare.gov’s eligibility guidelines, individuals and families can qualify for subsidies based on projected annual income when enrolling through the marketplace.

What Tanya didn’t know — and what the letter was trying to tell her — was that her income bracket, combined with the high benchmark premium in her county, meant she was entitled to a significantly larger credit than she’d received the year before.

Navigating the Enrollment Process as a Working Parent

Getting to that $491 figure was not simple. Tanya told me she spent portions of three evenings in December trying to update her enrollment through the federal marketplace portal, each time hitting a point where the system required income documentation she had to locate from prior-year tax filings.

She is the kind of person who keeps records — she showed me a labeled folder on her phone’s cloud storage — but cross-referencing her projected 2026 income as a flight attendant, which includes variable per diem pay, created confusion about what number to enter. Flight attendants often see fluctuating gross income depending on trip assignments, and Tanya’s base pay of $67,000 did not reflect the roughly $14,000 in additional per diem and incentive pay she typically earned.

She ultimately called the marketplace help line and spent 47 minutes on hold before reaching a representative who walked her through entering her income correctly and flagged that she had been under-reporting her credit eligibility the previous year as well. That detail landed quietly but heavily in the conversation between us.

“She said, ‘You may have left money on the table last year too,'” Tanya told me. “And I just felt this mix of relief and frustration. Relief because maybe this year is fixable. Frustration because I’ve been doing this for four years.”

The Student Loan Layer Nobody Talks About

Even with the insurance relief largely addressed, Tanya’s financial picture in early 2026 remained complicated. Her graduate degree — a Master of Science in Aviation Management from Embry-Riddle Aeronautical University, completed in 2020 — left her with $64,500 in federal student loan debt. Her monthly payment under an income-driven repayment plan had been recalculated at $718 following the reinstatement of federal student loan payments in late 2023.

Tanya told me she had looked into the Public Service Loan Forgiveness program but determined she didn’t qualify because her employer, a commercial airline, is a private company. She had also read about the SAVE repayment plan before it was paused by federal courts in mid-2024, an interruption that according to Federal Student Aid left many borrowers in limbo regarding their payment counts toward forgiveness.

“That was a gut punch,” she said. “I had restructured everything around that plan. And then it just… stopped.”

Where She Stands Now, and What She’s Still Watching

By the time we finished our coffee that Tuesday morning, Tanya had been on the corrected marketplace plan for about five weeks. Her first adjusted bill — $491 — had come through and cleared. She described it as a small exhale after months of holding her breath.

But the relief was measured. She told me she was watching two things closely: whether Congress would extend the enhanced ACA subsidies that have been periodically renewed since 2021, and what would happen to her income-driven repayment plan once the current legal battles around federal student loan rules resolved.

The enhanced premium tax credits she now benefits from are currently authorized through the end of 2025 plan year provisions, with ongoing legislative discussions about their continuation. If they lapse, Tanya’s premium would climb again — potentially back toward that $1,094 figure that sent her to her kitchen floor in January.

Driving back from our meeting, I kept thinking about the letter she almost recycled. There was no drama in how she found it — she just happened to clean the drawer before the holidays. Thousands of households in similar situations may have tossed theirs entirely, unaware that a form the government sent them contained, in dry bureaucratic language, a meaningful change to their monthly budget.

Tanya’s story isn’t a triumph. It’s a correction — a partial one, still fragile at the edges, depending on decisions made in Washington that she has no vote in. She’s hopeful, she told me as she gathered her things, but she said it the way people do when hope feels like a resource they’re rationing carefully.

Related: She Retired from USPS at 33 With a Spine Condition — Then Her Health Insurance Bill Hit $612 a Month

Leave a Reply