The first thing Monique Washington said when I sat down with her at a diner near her home in Baltimore was that she hadn’t slept a full night in three days. Not because of her route — she’s been driving for UPS for fourteen years and could do the job in her sleep. It was her brother, Darnell, 37, who’d had a bad stretch with his back. Her phone had rung at 2 a.m. twice that week, each time a home aide flagging something she needed to know.

I’d reached out to Monique after learning about her situation through a mutual contact at a Baltimore-area disability advocacy group. She agreed to talk, she said, because she was tired of being invisible. “People see me in my uniform and think I’ve got it together,” she told me. “They don’t see what’s behind the curtain.”

A Family Plan That Nobody Agreed To

When Darnell was 25, a driver ran a red light and hit the car he was riding in as a passenger. The crash left him with a traumatic brain injury and partial paralysis on his left side. He was in inpatient rehabilitation for nearly eight months. By the time he came home, their mother had quit her part-time job to care for him. Their father, already battling heart disease, died two years later.

Their mother passed in 2019 from a stroke. Monique, then 36, became Darnell’s primary caregiver by default — not by contract, not by legal arrangement, but by the quiet gravity of being the only one left.

Darnell qualifies for Social Security Disability Insurance (SSDI), which in 2025 paid him roughly $1,340 per month — slightly below the national average SSDI benefit of $1,537, according to the Social Security Administration. He also receives Maryland Medicaid, which covers doctor visits, prescriptions, and some home health aide hours. What it doesn’t cover is where Monique’s money goes.

The Gaps Medicaid Leaves Behind

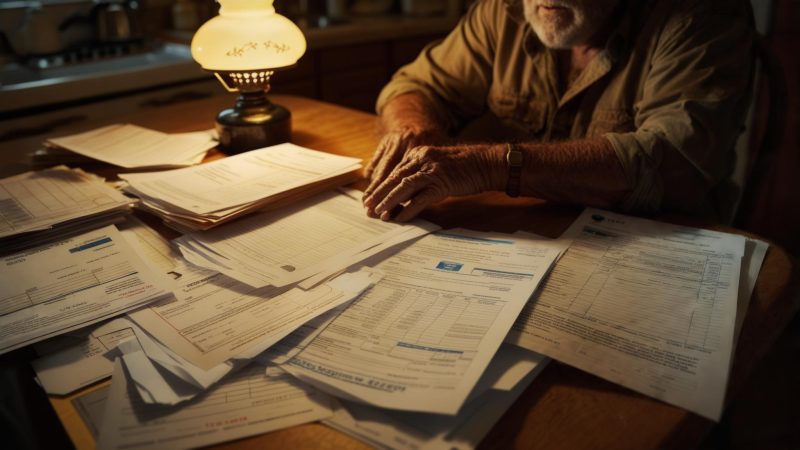

When I asked Monique to walk me through a typical month, she pulled out her phone and started reading from a notes app she uses to track expenses. The list was longer than I expected.

Darnell’s Medicaid-approved home aide covers 28 hours per week. His actual care needs — bathing, meal preparation, mobility assistance, medication management — require closer to 45. The remaining hours fall to Monique or to a private aide she pays $18 per hour out of pocket. On a heavy week, that’s an additional $306 she absorbs before a single other bill is paid.

Then there’s transportation. Darnell uses a wheelchair-accessible van service for medical appointments. Maryland’s Medicaid Non-Emergency Medical Transportation program covers rides to covered medical visits, but not to the twice-weekly physical therapy sessions his private physiatrist recommends — sessions that aren’t on Medicaid’s approved list. Monique pays for those rides herself, roughly $120 per month. The adaptive equipment — a specialized shower chair, a hospital-grade adjustable bed, a communication tablet his occupational therapist recommended — was purchased over three years using Monique’s credit card.

What Union Wages Can and Cannot Do

Monique’s position with UPS gives her something many caregivers don’t have: stable, well-compensated employment. As a full-time Teamsters-represented package car driver, she earns approximately $42 per hour under the 2023 master contract rates — a figure she confirmed for me, though she was modest about it. “People hear that and think I’m fine,” she said.

The math still doesn’t work in her favor. After taxes, her take-home pay runs around $5,400 per month. Her own mortgage, car payment, utilities, and groceries consume roughly $3,100. She estimates she spends between $500 and $700 monthly on Darnell’s uncovered needs — not including the months when something unexpected breaks down, a piece of equipment fails, or his condition requires a specialist visit that Medicaid won’t authorize.

What she hasn’t done in six years is contribute to her Teamsters 401(k). She stopped during the COVID-19 pandemic when her aide hours dried up and she was covering more herself. She never restarted.

She told me she’s thought about it. “Every time I get close to restarting, something happens. The van breaks, or there’s a new prescription he needs. I keep saying ‘next month.’ It’s been six years of next month.”

The Benefits She Didn’t Know She Could Access

Monique’s turning point — and it was more of a slow realization than a single moment — came in late 2024 when she attended a caregiver support meeting at a community center in her neighborhood. A social worker there told her about several programs she had never applied for because she didn’t know they existed for someone in her income bracket.

The first was Maryland’s Community First Choice (CFC) program, which operates under Medicaid and can expand personal care hours for eligible individuals. As Monique explained it to me, she had assumed Darnell’s 28 approved hours were the ceiling. They weren’t necessarily — the CFC program, she learned, allows for reassessments that can increase authorized hours based on documented functional need. She submitted a formal reassessment request in January 2025.

The ABLE account was the piece that made the most immediate practical difference. Under the IRS guidelines for ABLE accounts, eligible individuals with disabilities can save up to $18,000 annually (2024–2025 limit) in a tax-advantaged account without it counting against their asset limits for Medicaid or SSI. Monique had been informally holding money in her own savings account to cover Darnell’s expenses — which created zero tax benefit for anyone and kept the money tangled with her own finances.

“Nobody told us that existed,” she said. “I’ve been doing this for years and nobody — not the social worker at the hospital, not the Medicaid office — nobody told us about an ABLE account.”

Where Things Stand Now — and What Hasn’t Changed

When I followed up with Monique in February 2026, the reassessment had come through. Darnell’s authorized aide hours increased from 28 to 35 per week — not the 45 he functionally needs, but a meaningful reduction in the gap Monique was personally filling. She estimates that saves her approximately $126 per week in private aide costs on the weeks it works out.

The Maryland Family Caregiver Support Program approved her for a modest respite care voucher — enough for one weekend of substitute care per quarter. She used the first one in October 2025. It was, she told me quietly, the first two-day stretch in six years where she didn’t have to be reachable.

What hasn’t changed is her retirement gap. She still hasn’t restarted her 401(k) contributions. The VITA-prepared tax return for 2024 identified a small Credit for Other Dependents — $500 — that she hadn’t claimed in prior years because she hadn’t known Darnell qualified. It wasn’t transformative. It was something.

She’s also still on the same shift she’s held for years — the one that ends early enough to relieve the aide in the late afternoon. She’s been passed over twice for a more senior route that pays better, because taking it would require a later finish time. “I bid on it,” she told me. “Then I withdrew the bid. You do the math.”

Before I left, I asked Monique what she wanted people to understand about her situation — not about policy, not about benefits, just about what her life is actually like. She thought about it for a moment longer than I expected.

Monique Washington is one of an estimated 53 million Americans providing unpaid caregiving to a family member. Most of them are women. Most of them have no formal support infrastructure. And most of them, like Monique, discovered too late that there were programs available — had anyone thought to tell them.

The diner was emptying out when we finished talking. She had a 5 a.m. start the next morning and a call to make to Darnell’s aide before she went to bed. She left a good tip, put on her coat, and walked out into the cold Baltimore night with the same quiet efficiency she brings to everything. There’s a word for people who carry what Monique carries. The word isn’t caregiver. It’s invisible.

Leave a Reply