The conventional wisdom says that families with two incomes and a homeowner’s deed are doing fine. That they have enough runway to absorb a car breakdown or a bad quarter. That government relief programs are for people in far worse shape. Rochelle Womack is living proof that this assumption is wrong — and has been wrong for years.

I first encountered Rochelle through a comment she left on a piece I published last December about SSI income thresholds and the families they exclude. She had written three short sentences that stopped me cold: “We make too much to qualify for anything. We make too little to actually afford anything. Nobody ever writes about people like us.” I reached out the same afternoon. She called back two days later, a little suspicious, a lot direct.

When I sat down with Rochelle Womack — over the phone from her home in Milwaukee’s Bay View neighborhood on a Tuesday morning in March 2026 — I had no idea how layered her situation had become. What started as a conversation about disability benefits turned into a portrait of a family holding together by sheer stubbornness.

The Middle-Income Trap Nobody Acknowledges

Rochelle and her husband Darnell have one child together: Marcus, 11, who was diagnosed with Level 2 Autism Spectrum Disorder in 2018. Marcus requires full-time support — he cannot be left unsupervised, attends a specialized school program, and sees both a behavioral therapist and an occupational therapist weekly. Darnell stepped back from full-time warehouse work in 2021 to serve as Marcus’s primary daytime caregiver, which cut the family’s household income from roughly $91,000 to approximately $78,000 annually.

Rochelle brings in around $52,000 a year as a dental assistant. Darnell picks up part-time work where he can, adding another $26,000 in a good year. That combined figure — $78,000 — disqualifies them from most federally-means-tested programs. But it does not, by any stretch, cover what Marcus actually needs.

According to the Social Security Administration, the maximum federal SSI benefit for a child in 2025 was $943 per month — but because Darnell has part-time income, Marcus’s household benefit was reduced to $847. That gap between $847 and $2,400 in actual monthly care expenses is not theoretical. It is a number Rochelle knows by heart.

What the Disability Benefit Covers — and What It Doesn’t

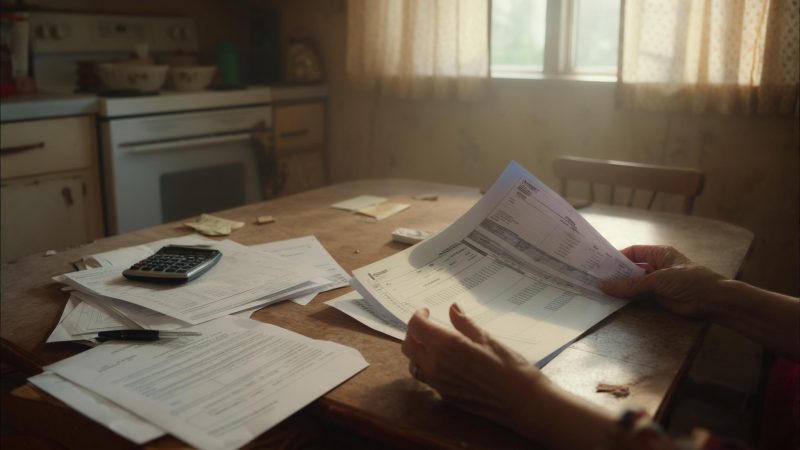

Marcus’s SSI check arrives on the second Wednesday of each month. Rochelle told me she cashed it and allocated it within the same afternoon: $320 toward his behavioral therapy co-pays, $210 toward specialized school supplies and adaptive equipment, $180 toward transportation to appointments, and the remainder absorbed into the general household shortfall. There is no surplus.

The therapists Marcus sees are not optional. His behavioral therapist has been working with him since 2019 and has helped reduce what Rochelle described as “meltdown cycles” from nearly daily to roughly once a week. The occupational therapist helps Marcus develop the fine motor skills he needs to eventually function more independently. Insurance covers portions of both, but the out-of-pocket co-pays for two speciality providers, seen weekly, add up to more than $600 a month before any other medical expenses.

What struck me most when Rochelle explained this was how long she had simply accepted it. “I never thought there was a way around it,” she said. “I thought that was just the number and you figure out the rest yourself.” That self-reliance — which she wore like a badge — had also kept her from exploring programs she might have partially qualified for.

When One Breakdown Becomes a Chain Reaction

In January 2026, Rochelle’s 2014 Honda Pilot developed a transmission problem that two separate mechanics estimated would cost between $3,100 and $3,400 to repair. She had $1,200 in savings — the result of months of careful rationing — and no line of credit she was willing to use.

The car is not a luxury. Marcus’s therapeutic school program is 14 miles from their home, with no accessible public transit route. Without the Pilot, Darnell has been relying on a borrowed car from Rochelle’s sister three days a week and paying for rideshares on the other days. Rochelle estimated that arrangement has cost the family an additional $380 per month since January.

She did not call a nonprofit. She did not look into emergency assistance programs. “That stuff is for people who are really struggling,” she told me, with a firmness that suggested she had said it to herself many times. I did not challenge her on it directly — but I noted that the family was spending more on the workaround than a structured assistance application might have taken to complete.

The Property Tax Problem She Didn’t Know Had a Solution

The $4,100 in overdue property taxes is the number that keeps Rochelle up at night. The family bought their Bay View home in 2016 for $187,000 — a modest purchase that has since appreciated significantly, which has also driven their annual property tax bill up to roughly $5,800. They fell behind during a difficult stretch in late 2024 when Darnell had a two-month gap in part-time work.

What Rochelle did not know — and what I spent part of our conversation walking through as reported fact, not advice — was that Milwaukee County has historically offered property tax installment plans for homeowners behind on payments, and that Wisconsin’s Homestead Tax Credit program provides direct relief to lower- and middle-income homeowners who meet adjusted gross income thresholds. The credit phases out at $24,680 in household income for most filers, which would exclude the Womacks — but a separate circuit-breaker provision for households with disabled dependents operates under different criteria.

When I mentioned the deferral option during our call, Rochelle went quiet for a moment. Then: “Nobody ever told me that existed.” She called the Milwaukee County Treasurer’s office three days after we spoke, she texted me to report. The installment deferral application was submitted on March 19, 2026. As of this writing, it is under review.

Where Things Stand Now — and What Rochelle Wants You to Understand

The Womack family is not in crisis by the metrics most assistance programs use. They own their home. Their income is above the median. Rochelle has health insurance through her employer. On a spreadsheet, they look stable. In practice, they are one larger emergency — a medical bill, a second car problem, a gap in Darnell’s work — away from something that spreadsheet cannot absorb.

The Child and Dependent Care Tax Credit, which Rochelle has claimed in prior years, provided a partial offset — roughly $1,200 back on their 2024 federal return, she estimated. The IRS guidelines allow families to claim up to $3,000 in qualifying expenses for one dependent, with a credit percentage that varies by income. For a family at the Womacks’ income level, the credit rate is among the lower tiers — another way the middle-income bracket loses on both ends.

What changed for Rochelle after our conversation was not dramatic. The property tax deferral is still pending. The car is still broken. But she started asking questions she had refused to ask before — not because she found faith in the system, but because the cost of not asking had quietly become higher than her pride.

I think about that line a lot. Rochelle Womack is not asking for rescue. She is asking to be counted — to be part of a conversation about economic relief that usually happens without people like her in the room. Her stubbornness is not a flaw. It is the only tool she has ever been given that reliably works. The question is whether the tools she has not yet been given might finally be worth reaching for.

Related: He Got a $9,000 Raise at 31 and Lost His SNAP Benefits the Same Month

Related: Your IRS Refund Status Says ‘Approved’ — That Does Not Mean the Money Is on Its Way

Leave a Reply