Roughly 1 in 5 eligible workers never claims the Earned Income Tax Credit — but for Claudette Zielinski, the problem wasn’t awareness. Someone else had already claimed it for her. When I connected with Claudette in early March 2026, she had just received a letter from the IRS that she’d been waiting on since February 2025. It sat on her kitchen table in Richmond, Virginia, unopened for two days before she could bring herself to read it.

Claudette had responded to a call-for-sources I posted on social media asking about families navigating government benefits under financial strain. Her message was brief: “I’ve been fighting the IRS for over a year because of identity theft. Nobody talks about what that actually does to a family living paycheck to paycheck.” We set up a video call, and she had her files spread across the table before I even said hello.

A Daycare, a Blended Family, and a Budget with No Slack

Claudette has run a licensed home-based daycare out of her Richmond rental since 2021. In 2024, her gross revenue was approximately $38,000 — enough to qualify for several federal credits but not enough to absorb a single financial shock. She and her husband have four children between them from prior relationships, ranging in age from 5 to 11.

Her husband’s ex-partner owes roughly $650 per month in court-ordered child support, a payment that hasn’t arrived consistently in over 18 months. That’s more than $11,700 in unpaid support by Claudette’s estimate — money the family had budgeted around when it was still coming in. “We stopped counting on it,” she told me, “but the bills didn’t stop counting on us.”

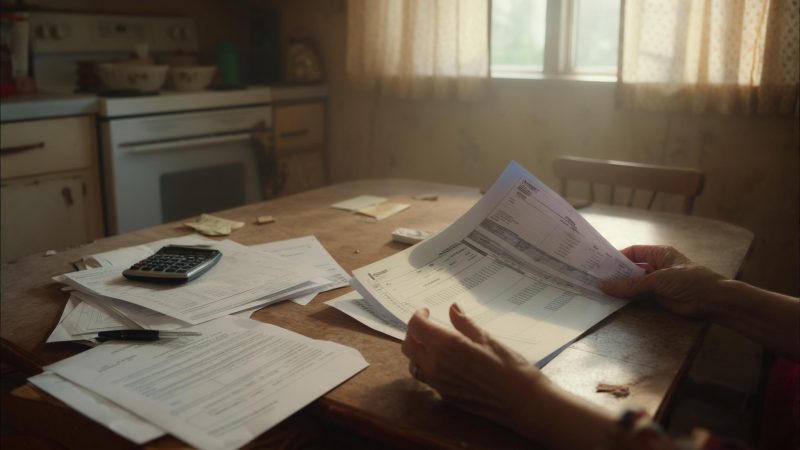

Claudette described herself as someone who takes a spreadsheet approach to finances — tracking every deduction, logging mileage for daycare supply runs, keeping receipts in labeled folders by month. But all of that discipline couldn’t protect her from what happened in February 2025, when she tried to e-file her 2024 federal return and received an immediate rejection notice.

The Moment the IRS Said Someone Else Had Already Filed Her Return

The rejection code was blunt: a return had already been submitted using her Social Security number for the 2024 tax year. Claudette told me she sat in her car in the daycare parking lot for twenty minutes before calling her husband. “I knew what it meant. I’d heard about it happening to other people. I just never thought it would be me — I don’t post my information anywhere, I shred everything.”

What she was dealing with is a form of tax-related identity theft that the IRS identifies as one of the most disruptive financial crimes facing individual filers. A fraudster had obtained her SSN — likely through a data breach she was never directly notified about — and filed a fabricated return to claim a refund before she could. The fraudulent return had already been processed.

She filed a paper return alongside IRS Form 14039, the Identity Theft Affidavit, in late February 2025. Her legitimate return included approximately $4,100 in Earned Income Tax Credit — calculated based on her income and four qualifying children — and roughly $2,100 in Child Tax Credit, bringing her total expected refund to about $6,200.

The Long Wait — and What It Cost Her

The IRS advises that identity theft cases can take 120 days or more to resolve. Claudette’s took significantly longer. From the date she submitted her affidavit to the date the IRS confirmed her case was resolved, 14 months passed. During that time, she received three form letters, two of which simply extended her wait time with no additional explanation.

While the refund sat frozen, Claudette made hard choices. She deferred a $1,200 repair on her daycare’s HVAC system through the summer months, running window units that drove her electricity bill up by roughly $180 per month. She also missed a $300 payment on a small business credit card, a delinquency that hit her already-damaged credit score — battered by the identity theft that had opened three unauthorized accounts in her name in 2023.

“Every time I thought I was getting ahead, something else fell apart,” she said. “And I couldn’t even be angry at myself because I did everything right. I just got unlucky, and unlucky is expensive.”

The Taxpayer Advocate Intervention That Changed Everything

The turning point came in September 2025, when Claudette — after reading about the IRS Taxpayer Advocate Service in an online forum for small business owners — submitted a request for case assistance. The Taxpayer Advocate Service is an independent organization within the IRS that handles cases involving significant hardship, and identity theft-related refund holds qualify for that designation.

Within six weeks of her TAS referral, Claudette said she received a direct phone call from a caseworker — her first human contact with the IRS in seven months. The caseworker confirmed that the fraudulent return had been flagged, that her legitimate return was being re-processed, and that she would receive her refund with statutory interest applied for the delay.

In January 2026, the IRS processed her legitimate 2024 return. In February 2026 — the same month she had first tried to file a year earlier — she received a direct deposit of $6,347. The extra $147 represented statutory interest the IRS added for the processing delay. She was also assigned an IRS Identity Protection PIN, a six-digit code now required on all her future returns that prevents anyone else from filing under her SSN.

What Claudette Has Now — and What’s Still Broken

When I asked Claudette what she did with the refund, she didn’t hesitate. “I paid off the credit card I missed while I was waiting. Then the HVAC repair. Then I put $800 away for the kids’ school supplies and summer camp fees.” The money that had felt abstract and bureaucratic for 14 months was gone within three weeks — absorbed by the debts that had piled up in its absence.

The unauthorized credit accounts opened in her name in 2023 are still on her report, still being disputed through the three major bureaus. Her credit score, which she said was around 680 before the identity theft, has not fully recovered. She’s working with a nonprofit credit counselor — a service she found through Virginia’s statewide financial literacy network — but she told me the process is slow and frustrating.

There’s also the matter of the unpaid child support. Claudette told me she and her husband filed a contempt motion through the Virginia Division of Child Support Enforcement in late 2025, but court backlogs have pushed their hearing to mid-2026. “We’re doing everything the right way,” she said, “and the right way just takes forever when you’re the one who can’t afford to wait.”

She’s already enrolled her IP PIN for the 2025 tax year filing. She keeps a dedicated folder for her 14039 paperwork, her TAS case number, and every letter the IRS sent — “just in case,” she said, with a short laugh that carried more exhaustion than humor.

What stayed with me after our conversation was something Claudette said near the end, almost as an aside: that the identity theft hadn’t just cost her $6,200 for 14 months. It had cost her the confidence that doing everything correctly would protect her. “I’m more careful than almost anyone I know,” she told me. “And none of that mattered.” That’s not a tax story. That’s a trust story — and the IRS still has some of that trust to earn back.

Leave a Reply