There is a particular kind of exhaustion that doesn’t come from having too little — it comes from watching a hard-won improvement quietly dissolve before you can hold onto it. When a social worker at Hennepin County’s public assistance office suggested I speak with Elaine Stanton, she described her in two words: “Resilient. Worn out.” Both turned out to be accurate.

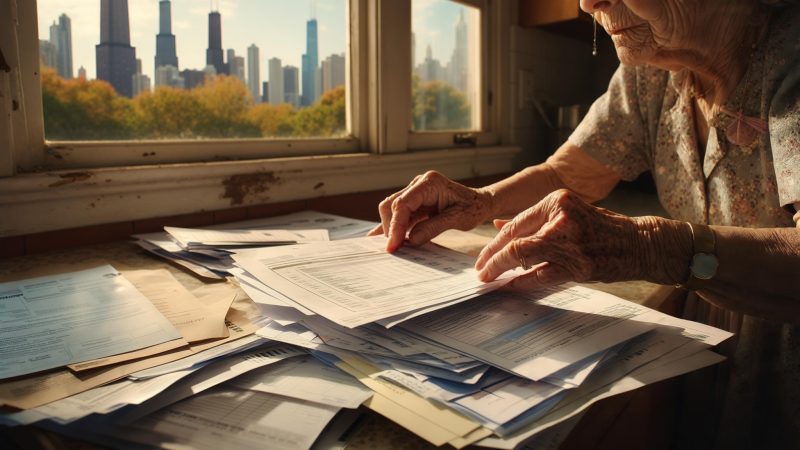

I met Elaine on a gray Tuesday morning in late February 2026 in the waiting area of a county benefits office in south Minneapolis. She was 53, recently divorced, and had come in to untangle a paperwork issue with the IRS that had been compounding since the previous fall. She wore pressed dental assistant scrubs and carried a manila folder thick with printed correspondence — letters from the IRS, credit bureaus, and the Federal Trade Commission. She had the look of someone who had explained her situation many times without resolution.

Over the course of two hours, Elaine walked me through eighteen months of financial turbulence — a story involving a well-deserved raise, a cascade of new expenses she hadn’t fully planned for, and an identity thief who exploited the moment her finances were most exposed.

A Raise That Did Not Feel Like One

In March 2024, Elaine received a raise at the dental practice where she has worked for eleven years. Her annual salary increased from $62,000 to $78,000 — a jump she described as “life-changing, at first.” She had been divorced for just over a year, was renting a one-bedroom apartment, and was, for the first time in years, operating in the black.

What followed was a pattern researchers sometimes call lifestyle inflation: expenses quietly expanding to absorb new income. Elaine moved to a larger apartment — $1,920 per month, compared to her previous $1,250. She financed a used car after her aging Civic finally gave out. She added a gym membership, meal delivery, and a monthly therapy co-pay she’d been skipping for years because she felt she couldn’t afford it.

None of those choices were reckless in isolation. Together, they meant her financial cushion never materialized the way she had imagined. “I looked at my bank account in November 2024 and I had maybe $1,100 saved,” she told me. “I was making sixteen thousand more dollars a year than I was two years ago. That made no sense to me.”

She began cutting back in December — canceling subscriptions, packing lunch, skipping the gym. Then, in the same month she was trying to course-correct, she got a letter from a credit monitoring service that stopped her cold.

When Identity Thieves Targeted Her at the Worst Possible Moment

In mid-December 2024, Elaine received a credit alert followed by a formal letter: three credit accounts had been opened in her name over the preceding six weeks, totaling approximately $14,200 in purchases. Someone had used her Social Security number, her real home address, and a slightly altered version of her email to pass identity verification at two major retailers and one financial services company.

Her credit score, which had been sitting at 718, dropped to 521 within sixty days. She filed a police report the same week, then spent the following month on hold with creditors, credit bureaus, and the FTC. But the crisis did not stay contained to her credit report.

When Elaine sat down to file her 2024 federal tax return in January 2025, she discovered that someone had already attempted to file a return using her Social Security number and claim a refund. The fraudulent return sought approximately $3,100. The IRS’s automated filters caught it before any payment went out — but the flag on her account meant that her legitimate return, and a real refund she was counting on, was now in a verification queue.

The Refund She Was Counting On Got Frozen

Elaine’s 2024 tax situation was straightforward on paper: single filer, no dependents, standard deduction, income from one employer. She had slightly overpaid withholding and expected a refund of approximately $2,740. As she told me, that money was already mentally allocated — toward the fraudulent debt she was disputing and a small emergency fund she was trying to build for the first time since her divorce.

Instead, the IRS refund tracker showed her return as “processing” for eleven weeks. She received Form 4883C — a letter requesting she verify her identity in person or by phone — which required her to call a specific IRS line and work through a lengthy verification process. It took three separate attempts before she connected with an agent who could process her confirmation.

While she waited, Elaine was also watching the news cycle around potential federal stimulus payments. The proposed $2,000 tariff dividend checks discussed publicly by President Trump had generated considerable attention, but as multiple outlets reported and the IRS confirmed, no such payment had been authorized by Congress as of early 2026, and the IRS had not announced any new federal relief payments for that period. “I wasn’t counting on any of that,” Elaine told me. “But I’d be lying if I said I didn’t check the news every couple of days hoping something had changed.”

What Actually Moved the Needle

The real turning point came in April 2025, when a caseworker at the county assistance office helped Elaine apply for an IRS Identity Protection PIN — a six-digit code the IRS assigns to identity theft victims that must accompany every future tax return. No one can file a federal return using her Social Security number without it.

Her $2,740 refund arrived via direct deposit in late March 2025 — about eleven weeks after she had originally filed. She put $1,200 toward a starter emergency fund and used the remainder to pay down a legitimate credit card balance she had been carrying since the divorce. No dramatic moves. Just steady ones.

“I didn’t do anything exciting with it,” she said. “I just tried to be boring for once. No decisions that felt exciting. Just steady.”

Where Elaine Stands Today — and What She Still Carries

When I spoke with Elaine in February 2026, her credit score had climbed back to 634 — not where it was before the theft, but functional enough to refinance her car at a lower rate. The three fraudulent accounts had been removed from two of her three credit reports; a dispute with the third bureau was still pending. Her emergency fund sat at approximately $2,100, and she had filed her 2025 return in January without any complications, using her IP PIN for the first time.

The exhaustion, though, had not fully lifted. “I feel like I spent an entire year being someone’s customer service problem,” she told me. “Every agency, every bureau, every IRS phone line. You have to be incredibly persistent, and persistence takes energy you don’t always have.”

She was measured about the future. She knew some people were still waiting on news of a federal stimulus payment — the proposed tariff dividend checks had circulated in headlines for months — but she had made peace with the uncertainty. “I can’t build a plan around something that might not happen,” she said. “I learned that the hard way.”

As I left the county office that morning, I kept thinking about how ordinary each piece of Elaine’s story was — a raise, some overspending, bad luck with a thief, a bureaucratic delay. No single element was catastrophic. Together, they nearly derailed two years of rebuilding. What pulled her through wasn’t a windfall or a stimulus check. It was documentation, patience, and the willingness to pick up the phone one more time when she would rather have given up.

Elaine Stanton is not finished rebuilding. But she is, unmistakably, still standing.

Leave a Reply