Roughly one in five eligible low-income families fails to claim the Child and Dependent Care Tax Credit each year, according to estimates from the IRS — leaving hundreds of millions of dollars in relief uncollected. I had read that statistic before. But I didn’t fully understand what it looked like in a real person’s life until I was standing in the vitamin aisle of a Walgreens on Southeast Hawthorne Boulevard in Portland, Oregon, on a gray Tuesday afternoon in late February 2026.

That’s where I first encountered Theresa Neville. She was at the pharmacy counter, her voice low but urgent, asking the pharmacist whether there was any program that could help reduce her son’s monthly medication costs. The pharmacist handed her a printed sheet and a phone number. Theresa folded it carefully into her coat pocket, like it was something fragile. I introduced myself, explained what I do, and asked if she’d be willing to talk. She looked at me for a moment, then said, “Sure. It’s not like I have anything left to be embarrassed about.”

A Career Cut Short, a Budget That Never Recovered

When I sat down with Theresa Neville at a coffee shop two days later, the first thing she told me was that she was not supposed to be in this position. She had done what she was told to do. She earned a graduate degree in public administration from Portland State University — graduating in 2022 with $34,500 in federal student loan debt — and landed a stable job as a postal service employee shortly after. She married her husband, Darnell, in the spring of 2023. Their son, Marcus, was born that December.

Marcus was diagnosed with a rare neurological condition before his first birthday. By early 2024, when he was still under a year old, it became clear that his care needs exceeded what any standard daycare could provide. Theresa left her position at the postal service in March 2024 — she was 24 years old. “I didn’t quit,” she told me carefully. “I just had to choose. And there was never really a choice.”

The household’s income dropped from approximately $52,000 annually to Darnell’s sole income of roughly $31,000 from his warehouse job. Marcus’s specialized care — a combination of a part-time in-home aide and therapeutic daycare two days per week — ran $1,400 per month. Student loan payments on Theresa’s $34,500 balance had resumed after the federal pause ended, adding another $310 per month. Their rent on a two-bedroom apartment in outer Southeast Portland was $1,650.

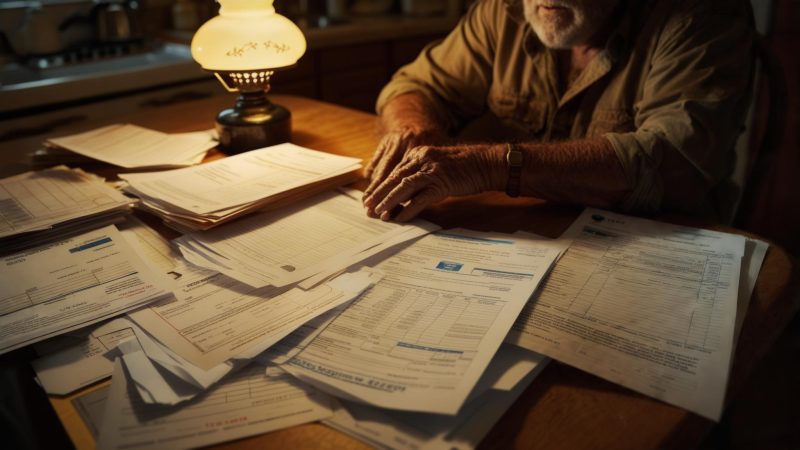

The math didn’t work. It hadn’t worked for nearly two years.

The Credits Nobody Told Her She Qualified For

The turning point began, unexpectedly, with a missed W-2. In January 2026, Theresa told me, she had decided not to file her 2025 tax return because she was convinced she owed money and couldn’t afford it. “We barely had anything going in,” she explained. “I figured the government didn’t owe me anything. I just wanted to stay out of trouble.”

A volunteer tax preparer through a local VITA (Volunteer Income Tax Assistance) site — which she’d found after the pharmacy encounter pointed her toward Oregon’s 211 information line — told her something that made her sit up straight in her chair. Her family likely qualified for the federal Child and Dependent Care Tax Credit, the federal Child Tax Credit, and Oregon’s Working Family Household and Dependent Care Credit.

Because Marcus’s care costs qualified as dependent care expenses — his providers were licensed and taxpayer-identified — a significant portion of that $1,400 monthly outlay was potentially creditable under federal rules. The IRS allows families to claim up to $3,000 in care expenses for one qualifying individual, or up to $6,000 for two or more. For lower-income households, the credit rate can reach up to 35 percent of qualifying expenses.

Oregon’s counterpart program — the Working Family Household and Dependent Care Credit — is specifically structured to benefit lower-income Oregonians, with enhanced rates for families below certain income thresholds. According to the Oregon Department of Revenue, the credit is refundable for qualifying low-income households, meaning it can generate a refund even when tax liability is zero.

What the Numbers Actually Looked Like

When Theresa sat down with the VITA preparer in early February 2026, the final numbers took shape. Between the federal Child and Dependent Care Credit, the federal Child Tax Credit, and Oregon’s refundable Working Family Credit, her estimated combined refund was approximately $3,200. She had never filed for any of it before.

I asked her what she did when she heard that number. She looked out the window of the coffee shop for a moment. “I called Darnell. I didn’t even say hello, I just said the number. He was quiet for so long I thought the call dropped.”

The combined refund represented more than one month of the family’s total household expenses. Theresa told me she wasn’t celebrating yet when we spoke — the return had been filed but not processed. “I’ve had things fall through before,” she said quietly. “I’m not buying anything until the money is actually in the account.”

A Small Win That Came With a Heavy Asterisk

That wariness runs through every part of Theresa’s story. She is 26 years old and describes herself, without bitterness, as someone who has made expensive mistakes. A series of late credit card payments during the chaotic first year of Marcus’s diagnosis had pulled her credit score down to 580. She had one medical collection account from an ER visit that cost $740 out of pocket after their coverage lapsed briefly during a gap between Darnell’s employer plans.

The student loan situation remained unresolved. Theresa’s $34,500 balance was in repayment, but she was on an income-driven repayment plan that set her monthly payment at $0 given the household income — technically helpful, but still accruing interest. “It’s like watching a hole in your boat get bigger while you’re bailing water,” she told me.

That mixture of hope and exhaustion is something I have encountered in varying forms in nearly every family I have reported on over the past several years of covering economic relief. The programs exist. The money is often real. But the distance between knowing a program exists and successfully navigating it — especially when you are also managing a child’s medical care, a stretched budget, and the residue of past financial mistakes — can be enormous.

What Theresa Wants Other Families to Know

Before we wrapped up our conversation, I asked Theresa what she wished she had known two years ago, when everything started unraveling. She thought about it for a long time.

“I wish I had known that not filing wasn’t protecting me. I thought if I didn’t file, nothing bad could happen. But by not filing, I was leaving money on the table that was supposed to help families like mine. Nobody told me that. Nobody ever said, ‘Hey, the system has something for you.’”

The VITA program she ended up using is free for households earning under $67,000 annually, according to the IRS VITA program page. Sites are available across Oregon and in most major metro areas nationwide. Theresa told me the preparer spent nearly two hours with her — something she said would have cost hundreds of dollars at a commercial tax office.

As I left the coffee shop that afternoon, Theresa was already on her phone — the Oregon 211 line, she told me, to follow up on that prescription assistance sheet from the pharmacy. The $3,200 refund hadn’t arrived yet. Marcus’s care costs hadn’t changed. The student loan balance was the same number it had been that morning.

But something had shifted. She knew what she was owed. That’s not nothing. For a lot of families I’ve reported on, that knowledge — arriving late and hard-won — is where the long climb back actually begins.

Related: Her Insurance Changed at 63 and Her Prescription Bill Nearly Tripled — Now She’s Racing the Medicare Clock

Related: She Filed on February 1 and Waited 61 Days: One Denver Family’s Tax Refund Became a Prescription Crisis

.pvv-faq-section details summary::-webkit-details-marker{display:none}.pvv-faq-section details summary::marker{display:none;content:””}.pvv-faq-section details[open] summary .pvv-faq-arrow{transform:rotate(90deg)}

Leave a Reply