Have you ever done everything right — worked hard, paid into the system for decades, played by every rule you knew — and still found yourself sitting across from a stack of government letters you couldn’t make sense of? That question was sitting in my head when I posted a call for sources on social media in late February 2026, asking whether anyone in the Pittsburgh area had navigated the maze of government benefits near or at retirement age. Nelson Parker responded within the hour.

We met at a diner on the South Side of Pittsburgh on a Tuesday morning in early March. Nelson arrived ten minutes early, ordered black coffee, and folded his hands on the table with the particular stillness of someone who has spent forty years solving problems with their hands and is now being asked to solve one with paperwork. He is 67 years old, widowed for four years, and still carries himself like a man who expects to fix whatever breaks. That instinct, it turned out, was both his greatest asset and the thing that nearly cost him.

Four Decades of Union Work — and a Retirement He Wasn’t Ready For

Nelson Parker spent 41 years as a licensed journeyman electrician with IBEW Local 5 in Pittsburgh. At his peak, he was pulling in roughly $82,000 a year in wages plus benefits — good union money, with a defined pension and health coverage that he rarely thought about because it was simply always there. He told me he had planned to work until 70, both because he genuinely liked the work and because the additional Social Security credits made financial sense.

That plan changed in September 2024 when a knee replacement surgery left him unable to safely work on elevated job sites. His union classified him as unable to perform full duties, and by November 2024 he had transitioned off the active payroll. He was 66 at the time — old enough for full Social Security retirement benefits, but not yet enrolled, because he had intended to delay. Suddenly, the timeline he had built his retirement around collapsed in about six weeks.

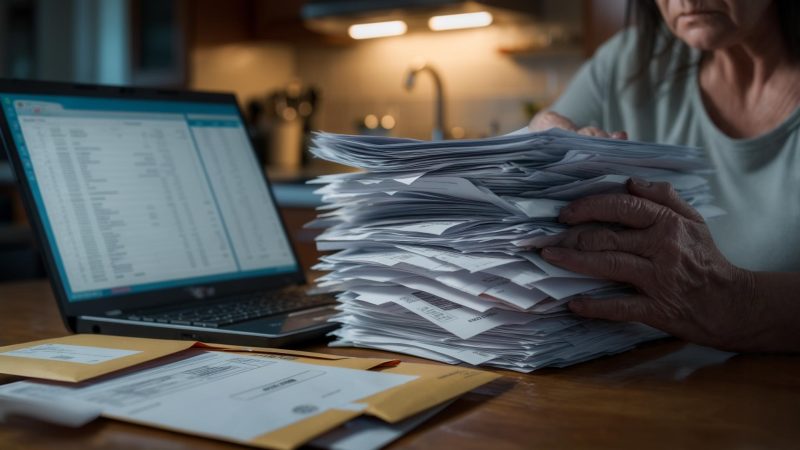

Nelson had already passed his 65th birthday, but because he had been on employer coverage continuously, he had a Special Enrollment Period to sign up for Medicare — a window he didn’t know existed and nearly missed. “Nobody tells you any of this,” he said, flattening his hands on the tabletop. “You think the union’s got you, and then the union’s gone, and you’re just a guy with a folder full of papers.”

The COBRA Bill That Was Higher Than His Rent

In December 2024, Nelson received his first COBRA election notice. The monthly premium to continue his union health plan under COBRA: $1,847. His rent for a two-bedroom apartment in Dormont, a neighborhood just south of Pittsburgh, was $1,190 a month. For roughly three months, he paid both — drawing down a savings account he had earmarked for emergency home repairs.

Between December 2024 and February 2025, Nelson spent approximately $11,400 on COBRA premiums alone. He enrolled in Medicare Part A and Part B in January 2025, which eventually allowed him to drop COBRA — but there was a roughly six-week processing delay during which he was paying both simultaneously. That overlap cost him an additional $3,694 out of pocket.

The Medicare transition itself created a new wrinkle. Nelson had not enrolled in Medicare Part D — prescription drug coverage — when he first became eligible at 65, because his union plan had creditable drug coverage. Once that union coverage ended, he had a 63-day window to enroll in Part D without a late enrollment penalty. He made the deadline by four days, something he found out only after calling the Medicare helpline three times over two weeks.

The Letter He Wasn’t Expecting: A Garnishment from the IRS

Nelson applied for Social Security retirement benefits in February 2025. His monthly benefit, based on his earnings record, was calculated at $2,614. He had delayed past his full retirement age of 66 and 8 months, so he received a modest delayed retirement credit bump. That number felt, briefly, like solid ground.

Then in April 2025, a letter arrived from the IRS. It informed him that a federal tax levy had been placed on his Social Security payments — $340 per month — stemming from an underpayment dispute going back to 2019. The issue involved a small remodeling side business he had operated for three years that, according to the IRS, had underreported self-employment income. Nelson maintained he had filed correctly based on what his accountant told him at the time. The dispute had been unresolved for years while he was still working and, in his words, “too busy to deal with it properly.”

According to the Social Security Administration, federal tax levies are among the few garnishments that can reduce retirement benefit payments. Nelson’s effective monthly income dropped from $2,614 to $2,274 — before Medicare Part B premiums of $185 were also deducted at source, leaving him with $2,089 per month to cover rent, food, utilities, and any out-of-pocket medical costs.

When the Car Broke Down, Everything Got Harder

I asked Nelson what the lowest point had been. He took a long sip of coffee before answering.

The Silverado was still sitting in a lot on the North Side when we met. Nelson had been borrowing his neighbor’s car two mornings a week for physical therapy appointments, paying her $40 per trip in gas money. He had priced out public transit routes to the orthopedic clinic — it would require two transfers and roughly 90 minutes each way, which his knee couldn’t manage yet. He told me this without complaint, as a logistical problem, not an emotional one. That was very much in keeping with how he described everything.

Nelson’s two adult children — a daughter in Phoenix and a son in Charlotte — had offered to help financially. He had turned them both down. “They’ve got their own kids, their own mortgages,” he said. “I’m not going to be that guy.” The self-reliance that had served him for four decades was now, in a quiet way, working against him.

On paper, Nelson’s numbers were not catastrophic. His union pension from IBEW Local 5 — approximately $1,340 per month after 41 years of contributions — provided a floor. But the combination of the COBRA bleed in late 2024, the ongoing garnishment, and a string of one-time costs had eroded roughly $19,000 in savings over 14 months. He estimated he had about $34,000 left in a money market account he had once thought of as a buffer, not a lifeline.

Where Things Stand Now — and What Remains Unresolved

By the time we spoke in March 2026, Nelson had made meaningful progress on some fronts and almost none on others. His Medicare coverage was stable. The COBRA overlap was behind him. He had filed an appeal with the IRS through a taxpayer advocate, a process he described as “filling out forms to get more forms,” but one that had at least temporarily reduced the levy from $340 to $170 per month while the dispute was under formal review.

The truck was still broken. He had resigned himself to budgeting the repair for May 2026, which meant six more weeks of borrowed cars and bus routes where the knee would allow. His daughter had driven up from Phoenix in February and stayed for a long weekend; he told me that was the first time he had asked for any help at all, and only because she had simply shown up and made it unavoidable.

The deeper issue, the one I kept returning to as I drove back across the river after our meeting, was not any single mistake Nelson made. He had not mismanaged money. He had not ignored warning signs. He had retired involuntarily, at the wrong moment, into a system that offers no orientation session and punishes gaps in knowledge as harshly as gaps in income.

Nelson Parker worked for 41 years in a trade that kept the lights on in hospitals, schools, and office buildings across western Pennsylvania. He paid into Medicare and Social Security for every one of those years. When I left the diner, he was still sitting at the table, refilling his coffee, turning over a folder of IRS correspondence like a man who has decided, against all evidence that it might be easier not to, that he is going to figure this out.

I believe him. That does not mean it should be this hard.

Related: My Husband Hid $42,500 in Debt. Then the IRS Seized Our Entire $4,200 Tax Refund.

Related: Brenda Counted on a $2,840 Tax Refund to Pay Off Medical Debt — Then the IRS Sent Her $1,190 Instead

Leave a Reply