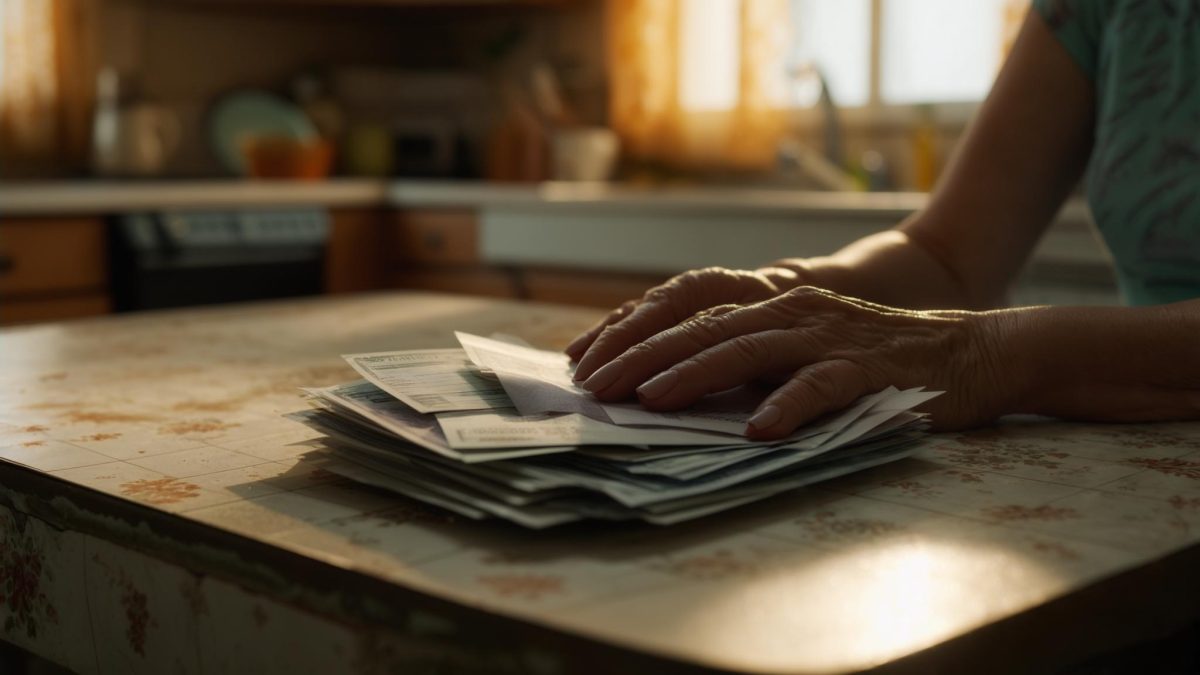

Roughly 40% of American households report they could not cover an unexpected $400 emergency expense without borrowing money — but the more invisible crisis belongs to families who earn too much to qualify for most safety nets and too little to absorb compounding shocks. When a community center in Spokane, Washington referred Crystal Novak’s story to our publication in February 2026, I wasn’t sure it would fit the usual narrative about financial hardship. She wasn’t destitute. She had a job, a spouse who worked, two healthy kids. What she had lost, quietly, was the margin.

I met Crystal on a Tuesday morning in the center’s resource room — a small, fluorescent-lit space with folding chairs and a coffee maker that had seen better years. She was punctual, wearing her bank name tag, having come directly from an early shift. She shook my hand firmly and said, almost by way of introduction: “I’m not sure my story is interesting enough for an article. It’s just a lot of small things that added up.”

A Year When Everything Moved in the Wrong Direction

Crystal Novak, 60, has worked as a bank teller at a regional financial institution in Spokane for eleven years. Her base salary sits at approximately $44,500 annually. Her husband Marcus works part-time as a delivery driver — roughly $29,000 last year. Together, they bring in around $73,500 before taxes, which places them in the upper-middle tier for Spokane’s cost of living. In most years, that was enough.

But 2025 delivered three separate financial hits in quick succession — none catastrophic alone, all of them corrosive together. When Crystal and Marcus’s lease renewed in March 2025, their landlord raised the monthly payment from $1,720 to $2,237, a 30% jump that added $517 to their obligations overnight. “We’d been there five years,” Crystal told me. “We thought that counted for something.”

Then came the insurance notice. In July 2025, Crystal filed a homeowner’s claim after a pipe burst in the unit below hers damaged stored belongings and shared structural space. The claim settled at $6,200. Two months later, her insurer — a regional carrier she’d paid premiums to for six years without incident — declined to renew her policy. Replacement coverage cost her an estimated $340 more per month than her prior premium.

The third hit was slower but perhaps the most demoralizing. For four years, Crystal had run a small mobile pet grooming business on weekends and evenings, licensed through Spokane County. At its peak in late 2023, the side operation brought in roughly $1,800 a month. By early 2025, that number had been cut nearly in half — down to around $900 — as two larger grooming chains opened nearby and fuel costs kept climbing.

Looking for Help in a System Built for Extremes

What Crystal described when I asked about seeking assistance was not dramatic — it was methodical, exhausting, and largely unrewarding. She started in October 2025 by reviewing what federal and state programs might apply to her household. As a bank teller, she understood financial products better than most. What she didn’t anticipate was how sparse the options are for households that don’t fall neatly into low-income categories.

The federal stimulus programs that had provided direct pandemic-era relief — three rounds of Economic Impact Payments — were long closed. According to Livemint’s IRS rebate tracker, no new general stimulus payment has been authorized as of early 2026, and the policy debate around a potential fourth check remains unresolved. Crystal had already claimed her Recovery Rebate Credit on her 2021 return. There was nothing new to collect.

Crystal looked into Washington State’s Working Families Tax Credit, a state-level refundable credit modeled on the federal Earned Income Tax Credit. She qualified for approximately $200 for tax year 2025 — meaningful, but not close to covering what she was losing each month. She also contacted the Washington State Department of Commerce about small business resources, finding mostly loan programs rather than grants, which she was reluctant to pursue given her tightened cash flow.

Her husband Marcus explored whether the business revenue decline might qualify them for any small business relief. Programs like Disaster Unemployment Assistance exist at the state level for workers affected by specific qualifying events — but the Novaks’ situation, a steady competitive decline rather than an acute declared disaster, didn’t fit those parameters.

The Emotional Weight of Being “Too Fine”

This is the part of Crystal’s story that a spreadsheet can’t capture. She earns enough that neighbors and coworkers assume she’s okay. The children are enrolled in school, the bills get paid — barely — and on the surface no crisis is visible to the outside world. That invisibility, she told me, carries its own weight.

Her two children, ages 11 and 10, know something has changed. The family stopped eating out entirely in the fall of 2025. A planned trip to visit Crystal’s sister in Portland was canceled. Marcus picked up two additional delivery shifts per week starting in November, adding an estimated $380 a month — but also compressing an already stretched schedule.

What struck me most sitting across from Crystal was the flatness in her voice when she described all of this. Not sad, not angry — flat. The community center coordinator who referred her story had used the word “resigned.” Sitting with her, I thought “numb” was more precise. She wasn’t catastrophizing. She was simply reporting the facts of her life the same way she might explain a checking account discrepancy to a customer.

What Crystal Found That Actually Helped

The turning point in Crystal’s story — such as it is — came not from a government program but from a workshop at the same community center where we met. In January 2026, a volunteer tax advocate through the VITA (Volunteer Income Tax Assistance) program helped Crystal reconstruct her small business deductions more thoroughly than she had in prior years.

By properly documenting vehicle mileage, grooming supplies, and a portion of her mobile phone costs as business expenses, Crystal’s taxable self-employment income dropped meaningfully. Combined with the Washington State Working Families Tax Credit and a federal Child Tax Credit claim for both children, her estimated 2025 federal refund came to approximately $1,840 — roughly $600 more than the year prior.

It wasn’t a rescue. $1,840 does not close a gap of $517 a month in rent plus hundreds more in replacement insurance premiums. But as Crystal put it: “It’s the first time in about a year where something went in the right direction. Even a little bit helps you feel less like you’re just watching things drain away.”

She is still in the same apartment, still paying the higher rent. The pet grooming business is still running at reduced capacity. The replacement insurance policy is still more expensive than the one she lost. None of the underlying pressures have resolved. What changed was Crystal’s grasp of what tools existed within the system she already lives in — and her willingness, finally, to let someone help her look.

What Crystal’s Story Reveals About the Relief Gap

Reporting Crystal’s story, I kept returning to the same tension: she earns enough to be excluded from most targeted assistance, but not enough to absorb stacked financial losses without consequence. It’s a category that doesn’t map cleanly onto most policy frameworks, and it’s larger than the data typically shows.

The wave of pandemic-era stimulus — including the $2.2 trillion CARES Act payments and subsequent rounds — reached broadly across income levels and helped households exactly like the Novaks weather short-term volatility. In its absence, the safety net has contracted back to means-tested programs that leave a significant swath of working Americans managing alone. According to Hindustan Times’ coverage of the Obama-era stimulus, even the 2009 American Recovery and Reinvestment Act — which beat its target of saving 3.5 million jobs — was a temporary intervention, not a structural fix for households caught in income squeezes outside declared emergencies.

Crystal isn’t waiting for a fourth stimulus check. She doesn’t believe one is coming, and she told me she had stopped following the policy news around it entirely. What she is doing — slowly, methodically, in the same measured way she manages everything — is rebuilding the margin, one small correction at a time. When I left the community center that Tuesday morning, she was already checking her phone for messages before her afternoon shift.

(function(){var w=document.getElementById(‘pvv-scenario-s1775653573786fhic’);if(!w)return;var btns=w.querySelectorAll(‘button[data-choice]’);btns.forEach(function(b){b.addEventListener(‘click’,function(){if(w.dataset.revealed)return;w.dataset.revealed=’1′;btns.forEach(function(x){x.style.opacity=x===b?’1′:’0.45′;x.style.cursor=’default’;x.style.transform=’none’});var o=document.getElementById(‘s1775653573786fhic-out-‘+b.dataset.choice);if(o){o.style.display=’block’}});b.addEventListener(‘mouseenter’,function(){if(!w.dataset.revealed){b.style.borderColor=’#38bdf8′;b.style.transform=’translateX(4px)’}});b.addEventListener(‘mouseleave’,function(){if(!w.dataset.revealed){b.style.borderColor=’#334155′;b.style.transform=’none’}})})})();

.pvv-faq-section details summary::-webkit-details-marker{display:none}.pvv-faq-section details summary::marker{display:none;content:””}.pvv-faq-section details[open] summary .pvv-faq-arrow{transform:rotate(90deg)}

Leave a Reply