I was waiting for a prescription refill at a Walgreens on Ingersoll Avenue in Des Moines last November when I heard a woman at the counter two spots down ask the pharmacist something that stopped me. “Do you know if there’s any kind of assistance program for people who had their hours cut?” She wasn’t loud about it. She was matter-of-fact, the way people get when they’ve already swallowed the embarrassment and are just trying to solve a problem.

That woman was Aisha Dawkins, 49, a home health aide who has spent the better part of two decades helping elderly and disabled clients in the Des Moines metro area get through their days. I introduced myself after she stepped away from the counter. She looked me over — the way someone does when they’re deciding whether talking to a journalist is worth their time — and then she shrugged. “Sure,” she said. “Maybe it’ll help somebody else.”

The Month the Budget Stopped Working

When I sat down with Aisha Dawkins at a diner near her home in early December, she laid out the timeline with the precision of someone who had gone over it too many times in her own head. For about three years, she had been pulling consistent overtime at her agency — usually an extra eight to twelve hours a week, which translated to roughly $480 a month after taxes. That money wasn’t a bonus. It was load-bearing.

Her husband, Marcus, works part-time at a logistics warehouse, bringing in approximately $1,200 a month. Aisha’s base pay runs about $2,650 a month. Together, before the overtime disappeared, the household was clearing just over $4,300 monthly — enough to cover a $1,050 mortgage, two kids in childcare, groceries, utilities, and a used Hyundai with 140,000 miles on it. Not comfortable. Functional.

In August 2025, the agency reduced available overtime hours agency-wide, citing rising administrative costs and a drop in Medicaid reimbursement rates from the state. Aisha’s extra shifts dried up almost overnight. “It wasn’t like they fired me,” she told me. “They just… stopped scheduling me past forty hours. And suddenly everything that was barely working stopped working entirely.”

She pulled out her phone and showed me a notes app where she tracks expenses by week. The math was blunt: by September, she was running a $390 monthly shortfall. By October, with a car repair eating up her small emergency fund, that gap had widened to nearly $600.

The Stimulus Rumor That Spread Through Her Circle

This is where the story gets harder to tell cleanly, because what happened next to Aisha is also happening to millions of Americans who are financially stressed and plugged into social media simultaneously.

Around October and November 2025, her Facebook feed and a neighborhood group chat started filling with posts about new stimulus checks — some claiming the IRS was issuing direct deposits tied to tariff revenue, others suggesting a new round of relief payments was imminent. According to reporting by FOX10 Phoenix, claims about new stimulus checks, IRS direct deposits, and tariff dividends circulated widely throughout 2025 — most of them unverified or outright false.

Aisha is not naive. She runs a side hustle reselling thrifted goods on Facebook Marketplace, tracks her own expenses obsessively, and has navigated Medicaid enrollment for three clients at work. But she told me that when you’re already $390 short every month and someone in your group chat says “my cousin got $1,400 deposited last week,” it’s very hard not to at least look into it.

What she found on the official IRS website was a portal for checking payment status — but no new round of stimulus checks authorized as of her searches in October or November 2025. The tariff dividend claims circulating on social media, including videos with titles like “2026 tariff stimulus” that were spreading rapidly, had no basis in any enacted legislation she could locate.

What She Actually Qualified For

Aisha didn’t give up when the stimulus rumors turned out to be dead ends. That restlessness — the same trait that keeps her running a side hustle on top of a full-time caregiving job — pushed her to keep looking for legitimate options. Over three months, she pieced together a picture of what was actually available to her family.

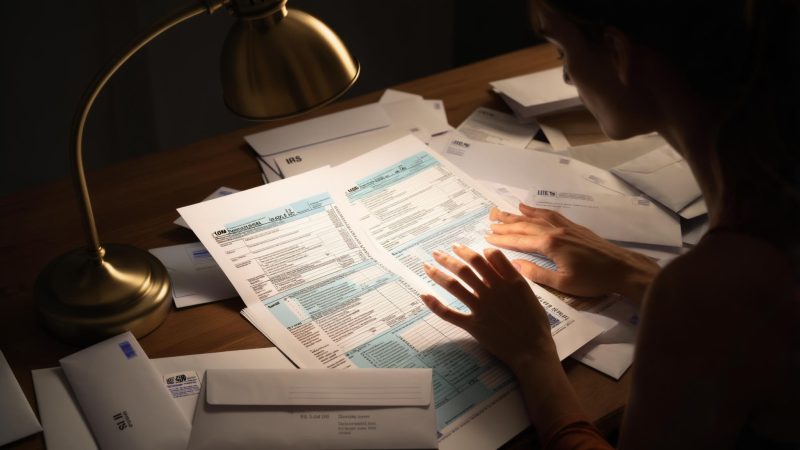

First, she revisited her tax filing situation. Because her household income had dropped with the overtime loss, she recalculated her estimated Earned Income Tax Credit eligibility for tax year 2025. Based on her projected income of approximately $46,000 for the year and two qualifying children, she estimated she could receive a meaningfully larger EITC refund than in prior years — potentially in the range of $3,500 to $4,200, depending on final income figures.

Second, she enrolled her younger child — the three-year-old — in Iowa’s Child Care Assistance program, which she had previously been over the income threshold to qualify for. With her reduced annual income, she now met the eligibility cutoff. That subsidy reduced her monthly childcare cost from $740 to approximately $290.

The Refund That Actually Arrived

When I followed up with Aisha in late February 2026, she had received her tax refund — $4,180 in total, combining her Earned Income Tax Credit and Child Tax Credit. It landed in her checking account on February 14th, a date she noted with a dry laugh. “Valentine’s Day,” she told me. “Marcus said the government finally sent us something.”

The refund didn’t solve everything. It covered the car repair backlog, brought her emergency fund back to about $800, and let her pay down a $1,200 balance she had run up on a credit card during the worst months of the shortfall. But it was not a windfall. It was a catch-up.

Her monthly budget is still tight. The childcare subsidy brought her monthly deficit from roughly $390 down to around $60 — close enough to manageable that her side hustle on Facebook Marketplace, which pulls in $150 to $300 a month depending on what she finds at estate sales, can cover the gap. She’s also back on a waitlist at her agency for any overtime that opens up.

What Aisha’s Story Reveals About the Gap Between Rumor and Reality

Sitting across from Aisha, I kept thinking about the cost of misinformation that isn’t malicious in the obvious sense — nobody pickpocketed her. But the weeks she spent researching viral stimulus claims were weeks she wasn’t spending applying for programs that actually existed. That gap has a price.

She’s not the only one. The speed with which unverified stimulus claims spread on social media — through Facebook posts, short-form videos, and group chats — means that financially stressed Americans are regularly navigating a landscape where the signal-to-noise ratio is brutal. The people most likely to see and act on those claims are often the people with the least margin for wasted effort.

When I asked Aisha what she would tell someone in her situation — someone who had just taken a financial hit and was seeing stimulus check rumors flood their social feeds — she paused for a long moment before answering.

As of early April 2026, Aisha is still working at the same agency, still running her Marketplace side hustle on weekends, and still keeping that weekly expense tracker on her notes app. Her seven-year-old started a free after-school program in January that removed another $80 a month from the budget. She’s not ahead. But she’s not behind anymore — and for now, that’s the line she’s trying to hold.

I left our second conversation thinking about what it costs — in time, in hope, in decision-making energy — to chase relief that doesn’t exist while real programs go unfound. Aisha found her footing, but it took her three months and a chance conversation at a pharmacy counter. Most people don’t have a reporter standing two spots down the counter.

(function(){var w=document.getElementById(‘pvv-scenario-s1775661509169iisl’);if(!w)return;var btns=w.querySelectorAll(‘button[data-choice]’);btns.forEach(function(b){b.addEventListener(‘click’,function(){if(w.dataset.revealed)return;w.dataset.revealed=’1′;btns.forEach(function(x){x.style.opacity=x===b?’1′:’0.45′;x.style.cursor=’default’;x.style.transform=’none’});var o=document.getElementById(‘s1775661509169iisl-out-‘+b.dataset.choice);if(o){o.style.display=’block’}});b.addEventListener(‘mouseenter’,function(){if(!w.dataset.revealed){b.style.borderColor=’#38bdf8′;b.style.transform=’translateX(4px)’}});b.addEventListener(‘mouseleave’,function(){if(!w.dataset.revealed){b.style.borderColor=’#334155′;b.style.transform=’none’}})})})();

.pvv-faq-section details summary::-webkit-details-marker{display:none}.pvv-faq-section details summary::marker{display:none;content:””}.pvv-faq-section details[open] summary .pvv-faq-arrow{transform:rotate(90deg)}

Leave a Reply