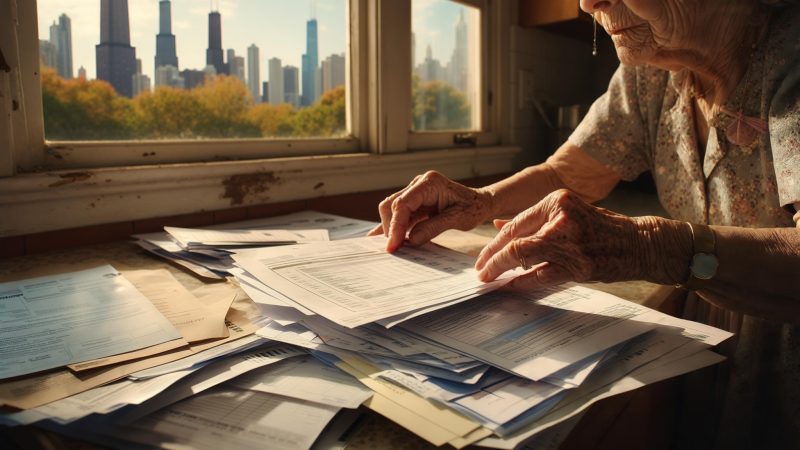

The community center coordinator who referred Lucille Gutierrez to me warned me ahead of time: she would show up with a folder. Sure enough, when I met Lucille at the Bethany Community Resource Center in Oklahoma City on a gray Tuesday in March 2026, she set a color-coded accordion file on the table before she even took off her coat. Inside were lease renewals, insurance denial letters, utility bills, and a handwritten budget spreadsheet going back to 2023.

Lucille is 67 years old. She spent 28 years as a mail carrier and postal clerk for the United States Postal Service before retiring in 2019. She is soft-spoken, precise with numbers, and, as she told me almost immediately, someone who has not slept more than five consecutive hours in the past four months.

A Fixed Income That Suddenly Wasn’t Enough

Lucille’s monthly income is predictable, which used to feel like a comfort. She receives approximately $1,420 per month in Social Security retirement benefits and $427 per month from her USPS civil service pension — a combined $1,847 a month. Her husband David, 68, had been supplementing the household with a part-time retail position that brought in roughly $620 a month. It was modest, but together they were managing.

Then, in January 2026, David was laid off when the hardware store where he worked closed its Oklahoma City location. That $620 was gone immediately. At nearly the same moment, the couple received their lease renewal notice for the two-bedroom apartment they have rented in the Warr Acres neighborhood since 2021.

Their rent had been $890 a month. The renewal set it at $1,157 — a jump of $267 per month, effective March 1, 2026. Lucille pulled out the original lease document from her folder to show me. The math she had written in pencil in the margin — old rent versus new rent, circled twice — was still there.

As Lucille explained it to me, the rent increase alone would have been manageable if David were still working. Together, they would have been tight but functional. Without his income, the couple was looking at housing costs consuming more than 62 percent of their total monthly take-home — well above the federal threshold of 30 percent that HUD defines as the boundary between affordable and cost-burdened housing.

The Insurance Letter That Arrived at the Worst Time

The rent notice was not the only blow that winter. In November 2025, Lucille filed a claim with her renter’s insurance provider after a pipe burst in their bathroom, causing roughly $2,400 in damage to flooring and personal belongings. The claim was paid. Then, in February 2026, she received a non-renewal notice from the insurer.

She was not behind on premiums. She had held the policy for four years without a prior claim. The non-renewal letter cited the single claim as sufficient grounds under the company’s underwriting guidelines.

Lucille told me she spent three evenings trying to get replacement coverage. Every quote she received was significantly higher than what she had been paying — one came in at nearly double her prior premium. She ended up going without coverage for the first time in her adult life. “I told David I felt like I was walking around without shoes on,” she said.

Finding Out What Was Available — and What Wasn’t

It was a caseworker at the Bethany Community Resource Center — the same person who eventually connected Lucille with my publication — who first suggested she look into federal and state assistance programs she had never considered. Lucille’s instinct, she told me, had always been that those programs were for people worse off than her.

The caseworker walked Lucille through a benefits screening in late February 2026. Several programs came up as potential matches based on the household’s income and circumstances.

Lucille applied for SNAP in early March 2026. The process took approximately 11 days from initial application to determination. Her household was approved for $186 per month in nutrition benefits — not a large sum, but enough to meaningfully relieve pressure on the grocery line of her monthly budget. “That’s $186 that can go somewhere else now,” she told me flatly. She was not celebratory about it. She was relieved in the way a person is relieved when a headache finally fades.

The Relief That Came Through — and the Gap That Remained

The LIHEAP application moved more slowly. Oklahoma’s LIHEAP program, funded through the federal Department of Health and Human Services, operates on an annual cycle with limited funding that is distributed until exhausted, according to OKDHS program guidance. Lucille submitted her application on March 4, 2026 — weeks after the peak winter assistance period — and was placed on a waitlist.

The Medicare Extra Help application was the clearest win. Lucille had been paying $38.40 per month for her Part D prescription plan and covering a $47 monthly copay for one of David’s medications out of pocket. After the caseworker helped her file for the Low Income Subsidy through the Social Security Administration, her Part D premium was reduced to zero and the copay dropped to $4.15. The combined savings came to roughly $81 a month.

The rental assistance program was a different story. The Oklahoma Housing Finance Agency’s emergency rental assistance funding had been largely depleted by the time Lucille’s caseworker reached out on her behalf. There was no active funding round accepting new applications in March 2026. Lucille’s name was added to a notification list for whenever the next allocation opened, but she was told not to count on anything within 60 days.

Where Things Stand — and What Lucille Wants Others to Know

When I met with Lucille in March 2026, she and David had been in their new lease for just over three weeks. The higher rent was being paid. The SNAP benefits were active. The Medicare savings were in effect. The LIHEAP assistance had not arrived. The insurance replacement gap was still unresolved — she was paying $94 a month for a bare-bones policy she found through the Oklahoma FAIR Plan, which she described as “better than nothing, which is what I had.”

The net effect of the programs that came through was approximately $267 per month in combined savings and new benefits — almost exactly the dollar amount of the rent increase. It did not make Lucille whole. It did not replace David’s income or restore the insurance coverage they lost. But it closed a specific, concrete gap at a moment when the gap felt unsurvivable.

As Lucille closed her folder at the end of our conversation, she said something that stayed with me. “I spent 28 years delivering people’s mail. I was a federal employee. I thought I understood how the government worked. I had no idea how many of these programs existed, or that I would ever be sitting somewhere filling out paperwork for them.” She paused. “I’m glad I did, though. I’m glad someone told me to look.”

She is still waiting on LIHEAP. She is still watching David’s job search. She still wakes up at 3 a.m. and does math in her head. But she is also, for the first time in months, doing that math with slightly different numbers — and some of those numbers are finally working in her favor.

Related: When Overtime Vanished and Rent Jumped $380 a Month, One Restaurant Manager Found Help She Didn’t Know Existed

Related: Darlene Filed Her Taxes in January. Her $3,400 Refund Didn’t Land Until April — Here’s What Delayed It

Leave a Reply