The call that started this story came from a comment section. Last November, I published a piece about workers who fall into coverage gaps after on-the-job injuries, and within hours a comment appeared beneath it — blunt, a little raw, and unlike most of the responses I usually get. “This happened to me,” wrote someone called AishaJ_Boise. “I got hurt, they denied me, and now I’m trying to figure out how to keep the lights on. Nobody talks about what comes after the denial.”

I reached out the same afternoon. A week later, I was sitting across from Aisha Jeffries, 50, at a kitchen table in her home on the east side of Boise, Idaho, a cup of coffee going cold between us while she walked me through the worst year of her adult life.

A Routine Day That Changed Everything

Aisha has worked as a home health aide for nearly twelve years. The job pays irregularly — her hours vary week to week depending on client assignments, and her monthly take-home has ranged anywhere from $1,800 to $2,400 over the past two years. She is remarried, and her blended household includes children from both her and her husband Marcus’s previous relationships. Money is always tight. Surprises are always expensive.

On March 7, 2024, Aisha was helping an elderly client in a private residence in Garden City when she slipped on a wet bathroom floor and fell hard on her left knee and hip. “I heard something pop,” she told me. “I knew right away it wasn’t just a bruise.”

She filed a workers’ compensation claim through her employer’s insurer within 48 hours, exactly as she had been told to do. The injury was documented at an urgent care clinic that same evening — partial medial meniscus tear, hip contusion, restricted mobility. Her physician recommended six to eight weeks of limited duty. The insurer’s adjuster contacted her ten days later and asked her to submit to an Independent Medical Examination (IME).

On May 19, 2024, she received a denial letter. The insurer’s position was that the injury could not be “conclusively attributed” to a workplace incident, citing the IME physician’s report. Aisha had no attorney. She had no idea she could appeal. And she had $14,200 in medical bills that were now entirely her responsibility.

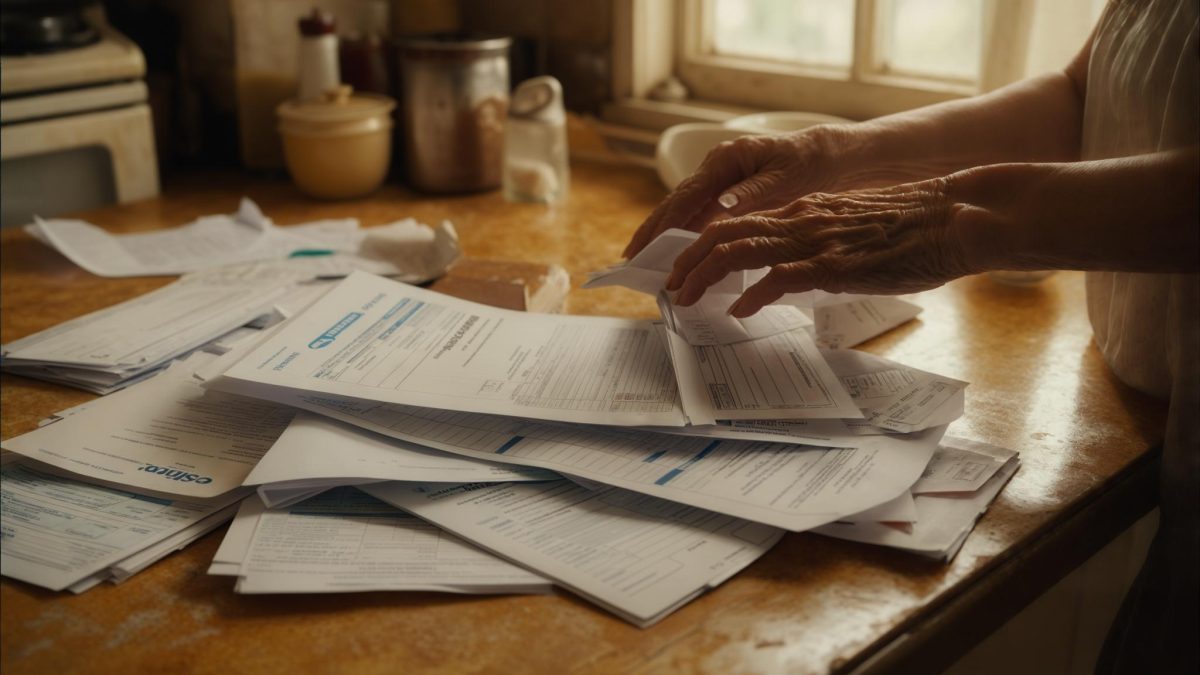

The Financial Spiral Nobody Warned Her About

What followed the denial was not a single crisis — it was a chain reaction. Aisha told me she tried to manage the medical bills herself at first, making small payments to keep the accounts from going to collections. But her irregular income made that nearly impossible to sustain.

By August 2024, two of the medical accounts had gone to collections. Her credit score, which had already carried some scars from earlier financial mistakes, dropped from 620 to 547. A score that low closed doors she had not even tried to open yet — a personal loan to consolidate the bills, a balance transfer card, even a second job application that required a credit check.

She did not cut back on what she provided for her family during this period. That detail struck me when she mentioned it almost in passing. When I asked her about it directly, she shrugged. “My kids didn’t cause this,” she said. “Marcus’s kids didn’t cause this. I wasn’t going to make them feel it if I could help it.”

What She Found — and What She Missed

Aisha told me that she spent most of the summer of 2024 trying to research relief options on her own, mostly late at night after the household had gone to sleep. She found the process disorienting. “There’s so much information out there, but it’s not organized for someone like me,” she said. “I don’t know the right words to search. I don’t know which programs are real and which ones are scams.”

She eventually connected with a navigator at the Benefits.gov referral network who helped her apply for two programs she had not considered. The first was the Idaho Low Income Home Energy Assistance Program (LIHEAP), which helped cover a $310 utility bill that had been building since summer. The second was SNAP — the Supplemental Nutrition Assistance Program — for which her household qualified based on net income after medical expenses were factored in.

The SNAP approval was the first meaningful relief she received. Her household of five was approved for approximately $840 per month in food benefits beginning in October 2024. “That was the first time in six months I felt like I could breathe a little,” she told me.

The Thing She Didn’t Know — and Still Regrets

When I told Aisha that she had likely had the right to appeal the workers’ comp denial within 60 days of the May 2024 letter, she went quiet for a moment. According to the Idaho Industrial Commission, workers can request a formal hearing before a referee — and if they prevail, they may be entitled to medical cost reimbursement and partial wage replacement dating back to the injury. That window closed in July 2024. Aisha had no idea it existed.

This is not unusual. A Government Accountability Office review of workers’ compensation systems has found that low-wage workers in personal care and home health occupations have among the lowest appeal rates of any occupational group — not because their claims are more often correct, but because they are less likely to know their rights and less able to take time off work to pursue them.

Aisha’s situation also illustrates a gap that rarely gets discussed: what happens financially in the months between a denial and any potential relief. There is no bridge program. There is no automatic referral to SNAP or LIHEAP when a workers’ comp claim is denied. Workers are simply left to navigate it themselves, often while still physically injured and still working reduced hours.

Where Things Stand Now

When I spoke with Aisha again in late March 2026, she had made some progress — though she was careful not to call it a recovery. One of the two collection accounts had been negotiated down from $4,800 to $2,100 through a debt settlement arrangement she found through a nonprofit credit counseling service. The second remains open. Her credit score has climbed to 571.

Her knee still aches in cold weather. She still works irregular hours — sometimes thirty a week, sometimes forty-five, rarely anything she can count on. Marcus took on a second part-time job last fall to help stabilize the household income. “He shouldn’t have had to do that,” she told me, and the way she said it made clear she carries that as a personal weight, not just a logistical fact.

What she wants people in her situation to understand — and what she told me directly — is that the denial letter is not the end. It feels like the end. The language is formal and final and nobody calls you back. But the process has more steps, and the people who know about those steps usually aren’t the ones handing you the bad news.

Sitting with Aisha in her kitchen, watching her talk about her blended family with a warmth that didn’t match the difficulty of everything she had just described, I kept thinking about how much of her situation came down to information — what she knew, what she didn’t, and how much the gap between those two things costs people who can least afford it. That is not a lesson with a tidy resolution. It is just the truth of what I found when I followed up on a comment in a comment section, and it is the reason she agreed to tell her story.

Related: COBRA Was Costing This El Paso Couple More Than Their Rent. Then the 60-Day Enrollment Window Almost Slammed Shut.

Related: She Was Counting on a $2,400 Tax Refund After Her Workers’ Comp Was Denied — Then the IRS Put Her Refund on Hold

Leave a Reply